Introduction

As the tax filing season is emerging. We Individuals may have incomes from country outside India also. It is important to know about Double Taxation Avoidance Agreement (DTAA) as we may end up paying tax on the same income in both the countries.

India has signed DTAA agreement with over 90 countries to ensure that taxpayers do not pay tax twice on the same income. This DTAA provisions are helpful to taxpayers who are Residents in India and earn incomes from countries outside India.

What is DTAA?

In the present era of cross-border transactions, the effect of taxation is one of the important considerations. When a taxpayer is a resident in one country and earns income outside India it gives rise double taxation relief. This arises from the two basic rules that enables the country of residence as well as country where the source of income exists to impose tax namely (i) the Source Rule and (ii) the Residence Rule.

Source Rule of Taxation : Income to be taxed in the country in which it originates irrespective of the whether income accrues to a resident or non-resident.

Residence Rule of Taxation : Power to tax the income should rest with the country in which the taxpayer resides.

DTAAs lays down the allocation rules for taxation of income by the source country and the residence country.

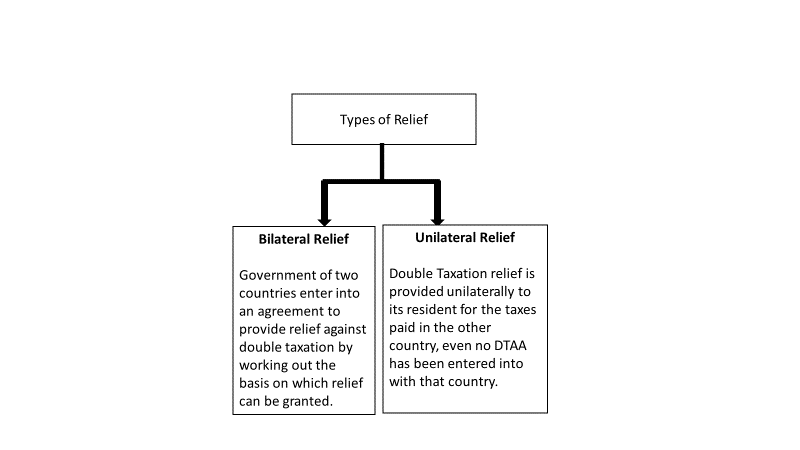

Types of relief

There are two types of relief namely :

- Bilateral Relief; and

- Unilateral Relief

DTAA provisions under Income Tax Act

Agreement with foreign countries or specified territories outside India / Adoption by Central Government of agreement between specified associations for double taxation relief – Bilateral Relief [section 90/90A]

Section 90/90A provides bilateral relief for double taxation. Section 90 empowers the Central Government to enter into an agreement with foreign country or specified territory outside India while Section 90A empowers the Central Government to make provisions for adopting and implementing of any agreement entered by any specified association in India with any specified association in the specified territory outside India.

Objective of agreement under section 90 or 90A

- For granting of relief in respect of :

- income on which tax has been paid in India and the other country or specified territory; or

- income tax chargeable under this Act and under the tax laws force in that country or specified territory to promote mutual economic relations, trade and investment; or

- for the avoidance of double taxation of income under this Act and under the corresponding law in force in that country or specified territory, as the case may be, without creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance (including through treaty-shopping arrangements aimed at obtaining reliefs provided in the said agreement for the indirect benefit to residents of any other country or territory), or

- for exchange of information for the prevention of evasion or avoidance of income-tax chargeable under this Act or under the corresponding law in force in that country or specified territory, as the case may be, or investigation of cases of such evasion or avoidance, or

- for recovery of income-tax under this Act and under the corresponding law in force in that country or specified territory.

The Central Government vide Notification No.90/2008 dt 28.08.2008 and Notification No. 91/2008 dt 28.08.2008 notified that where an agreement under section 90/90A for granting of relief of tax or avoidance of double taxation provides that any income of a resident of India may be taxed in other country, then such income shall be taxable in India also according to the provisions of the Income Tax Act, 1961 and relief shall be granted in accordance with the method for elimination or avoidance of double taxation.

Documents required to be furnished by the assessee for claiming treaty benefits:

- Status (individual, company, firm etc.) of the assessee;

- Nationality (in case of an individual) or country or specified territory of incorporation or registration (in case of others);

- Assessee’s tax identification number in the country or specified territory of residence and in case there is no such number, then, a unique number on the basis of which the person is identified by the Government of the country or the specified territory of which the asseessee claims to be a resident;

- Period for which the residential status, as mentioned in the certificate referred to in sub-section (4) of section 90 or sub-section (4) of section 90A, is applicable; and

- Address of the assessee in the country or specified territory outside India, during the period for which the certificate, as mentioned in (iv) above, is applicable.

The assessee may not be required to provide the information or any part thereof referred to in sub-rule (1) if the information or the part thereof, as the

case may be, is contained in the certificate referred to in sub-section (4) of section 90 or sub-section (4) of section 90A.

Countries with which no agreement exists – Unilateral Relief [section 91]

Relief under this section is granted to a person when Income arises to a resident taxpayer from a country with which no DTAA agreement exist. To claim relief under section 90, the following conditions needs to be fulfilled:

- The assessee is a resident in India during the previous year in respect of which the income is taxable.

- The income accrues outside India.

- The income is not deemed to accrue or arise outside India during the previous year.

- The income accrued is subjected to tax in the foreign country in the hands of the assessee.

- The assessee has paid tax in the foreign country.

- There is no agreement for relief from double taxation between India and the other country where the income has accrued or arisen.

In these cases, the assessee shall be entitled to a relief from the tax payable by him/her in India. This deduction will be calculated on the doubly taxed income at the Indian tax rate and the rate of tax in the said country, whichever is lower.

Foreign Tax Credit [Rule 128 of the Income Tax Rules, 1962]

Year of availability of Foreign Tax credit

A resident taxpayer shall be allowed credit for the amount of tax paid in the foreign country or specified territory outside India, by way of relief in the year in which the income corresponding to such tax has been offered to tax in India.

If the income on which foreign tax has been paid or deducted is offered to tax in India for more than one year, then the credit of foreign tax (i.e relief) shall also be allowed in the proportion of income offered to tax in India.

Manner of computing Foreign Tax Credit

The credit of foreign tax would be the aggregate of the amounts of credit computed separately for each source of income arising from a particular country or specified territory outside India and shall be given effect in the following manner:

- The credit would be lower of the tax payable in India as per the provisions of the Income Tax Act 1961 and the tax paid on the income in the foreign country.

However, if the tax paid in the foreign country exceeds the amount of tax payable in India, then such excess amount shall be ignored. - The credit would be determined by conversion of the currency of payment of foreign tax at the Telegraphic Transfer buying rate (TTBR) on the last date of the month immediately preceding the month in which such tax has been paid or deducted.

How to Claim DTAA in your ITR?

Steps to follow to claim DTAA relief in your income tax return.

- Choose the correct ITR form

- Report the foreign income in Schedule FSI (Foreign Source Income)

- Claim Relief in Schedule TR (Tax Relief)

- Submit Form 67 before uploading the IT Return.

- Upload the necessary documents such as Form 1042S or Tax paid /deducted certificate from the foreign country while filing Form 67.