What are Sovereign Gold Bonds (SGBs)?

Sovereign Gold Bonds (SGBs) are government securities issued by the Reserve Bank of India (RBI) on behalf of the Government of India. Denominated in grams of gold, they provide investors with exposure to gold price appreciation without the need for physical possession, thereby eliminating risks such as storage, theft, and making charges associated with physical gold.

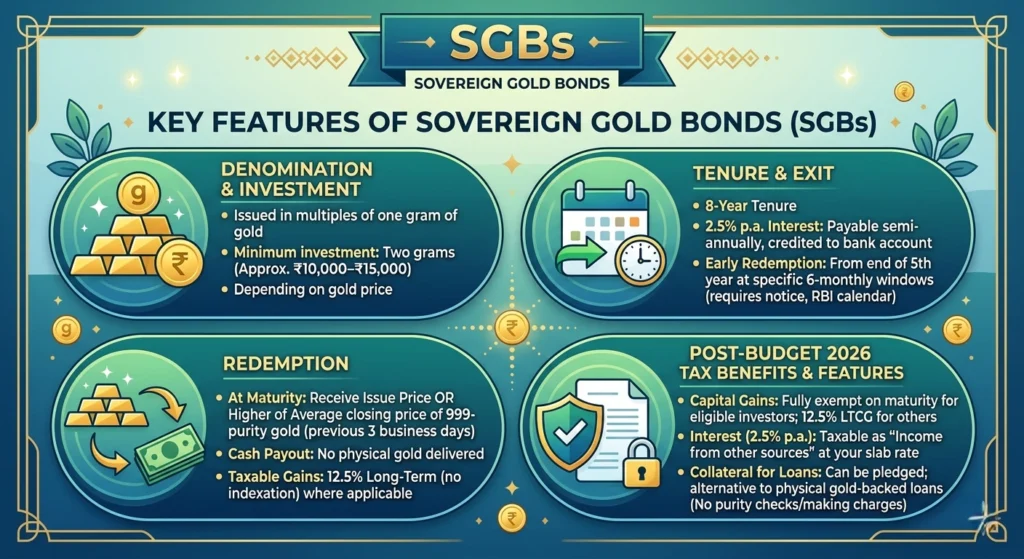

Key Features

The key features of SGBs are summarised below:

- Denomination and Investment

- Issued in multiples of one gram of gold, with a minimum investment of two grams (roughly ₹10,000–₹15,000, depending on the prevailing gold price at subscription).

- Tenure and Exit

- 8‑year tenure, with interest payable semi‑annually at 2.5% per annum, credited directly to your bank account.

- Early redemption is allowed from the end of the 5th year at specific 6‑monthly windows, subject to a few days’ notice and RBI’s early‑redemption calendar.

- Redemption

At maturity, investors receive the issue price or the average closing price of 999‑purity gold over the previous three business days (whichever is higher), paid in cash—no physical gold is delivered.

Taxable gains, where applicable, are taxed at 12.5% long‑term without indexation, similar to many other regulated instruments. - Tax Benefits (Post‑Budget 2026 overview)

- Capital gains: for eligible investors, gains on maturity can be fully exempt; for others, LTCG at 12.5% applies.

- Interest: the 2.5% annual interest is always taxable as “income from other sources” at your slab rate.

SGBs can be pledged as collateral for loans, offering a convenient alternative to physical gold‑backed loans without the hassles of purity checks or making charges.

Risks and Limitations of SGBs

While SGBs are safe and sovereign‑backed, they are not risk‑free:

- Gold‑price risk: If gold prices fall below your purchase levels, the redemption value can be lower than your entry cost, even though you still earn 2.5% interest.

- Lock‑in period: The effective horizon is 8 years, even though an early‑redemption window opens after 5 years; this limits flexibility for short‑term financial needs.

- Liquidity risk: Trading volumes on exchanges can be thin, so selling on the secondary market may be difficult or force you to accept a poor price.

- Issuance‑window risk: SGBs are issued only in specific tranches; if you miss a window, you may have to wait months for the next opportunity, and timing the launch date with gold levels can be tricky.

Who Can Invest in Sovereign Gold Bonds (SGBs)?

Eligibility for Sovereign Gold Bonds is straightforward and inclusive, designed to suit a wide range of investors while adhering to regulatory norms. Under the Foreign Exchange Management Act (FEMA), 1999, only persons resident in India qualify to invest. This covers:

- Resident Indians

- Individuals (including those investing on behalf of minors; the guardian signs the application).

- Hindus Undivided Families (HUFs), via the Karta.

- Institutions: trusts, universities, and charitable organisations.

- Non‑residents and NRIs

- NRIs cannot subscribe to new SGB issues; they are generally restricted from fresh investments.

- However, if you bought SGBs while you were a resident and later become an NRI, you can continue holding them until early redemption or maturity. Redemption proceeds will be paid to your NRO account, and interest and capital‑gains tax will apply as per your tax status.

Joint holdings are permitted, with applications in the name of the first applicant and up to three joint holders. Importantly, the maximum investment limit (4 kg for individuals/HUFs, 20 kg for trusts/institutions per fiscal year) applies to the first applicant for that specific tranche, regardless of joint ownership.

This structure ensures accessibility for families, small investors, and institutions alike, making SGBs a practical choice for diversified savings. Always verify the latest RBI guidelines during subscription periods for any updates.

How Budget 2026 Changed the Tax Rules for Sovereign Gold Bonds?

Sovereign Gold Bonds (SGBs) have long been one of the most attractive ways to invest in gold in India, combining the safety of a government‑backed instrument, an annual 2.5% interest payout, and fully exempt capital gains if held until maturity.

The Union Budget 2026 has significantly narrowed this tax advantage, making the tax treatment of SGBs highly dependent on how and when you bought the bond, rather than treating all investors the same.

Key Change: When Are SGB Gains Still Tax‑Free?

The core change lies in Section 70(1)(x) of the Income‑tax Act, 2025, which lists transactions not treated as “transfers” for capital‑gains purposes and had earlier treated all SGB redemptions with the RBI (on maturity or via premature‑redemption windows) as non‑taxable.

From 1 April 2026, the provision is effectively tightened to a narrow category:

Capital gains on SGB redemption will be fully exempt only if all three conditions are met:

- The investor is an individual (the benefit is not extended to HUFs, trusts, or institutions).

- The SGB was subscribed to at the time of original issue (via RBI, through banks, post offices, or demat, not via stock‑exchange trades).

- The bond is held continuously until redemption on maturity (8 years), with no premature redemption.

In this case, the appreciation on the bond at maturity remains tax‑free, though the 2.5% annual interest continues to be taxed as “income from other sources” at the investor’s slab rate.

Who Now Pays Capital‑Gains Tax on SGBs?

For everyone outside that narrow group, capital‑gains tax will generally apply from 1 April 2026 onwards. The key scenarios are:

1. Secondary‑Market Buyers (Exchanged‑Purchased SGBs)

If you bought SGBs on the stock exchange (not directly from RBI), the exemption no longer applies, regardless of how long you hold.

- Redemption on maturity after 1 April 2026: Gains will be taxed as long‑term capital gains (LTCG) at 12.5%, without indexation.

- Premature redemption (during the 6‑monthly windows after the 5th year) or sale on the exchange before maturity: Gains are also taxable as LTCG or STCG, depending on holding period.

2. Original Subscribers Who Redeem Prematurely

Even if you bought the SGB at original issue, if you redeem before maturity (i.e., through the early‑exit window after year 5), the gain will now be treated as taxable capital gains, not as an exempt non‑transfer.

This is a notable shift from the pre‑2026 regime, where premature redemption was also tax‑free for all investors.

3. Anyone Selling SGBs on the Exchange Before Maturity

Sales on the stock exchange prior to maturity were always taxable and remain so:

- Long‑term (>12–36 months, depending on latest holding‑period rules): LTCG at 12.5% without indexation.

- Short‑term (≤12–36 months): STCG taxed at the investor’s normal slab rate.

A Practical Example

Consider an investor who bought SGBs in the secondary market:

- Purchase price: ₹10,00,000

- Redemption value on maturity: ₹45,00,000

- Holding period: Long‑term (>12 months)

Before Budget 2026:

- Long‑term capital gain: ₹35,00,000

- Tax: Nil, because redemption‑linked gains were fully exempt.

After Budget 2026 (from 1 April 2026):

- Long‑term capital gain: ₹35,00,000

- Tax at 12.5%: ₹4,37,500

This illustrates why the tax‑free image of SGBs has clearly faded for secondary‑market investors.

Interest and Indexation: What Still Remains Unchanged?

- The 2.5% annual interest paid half‑yearly continues to be taxable as “income from other sources” at the investor’s slab rate. There is no change in this treatment introduced by Budget 2026.

- Indexation is not available on SGBs; indexation benefits for SGB‑linked gains were withdrawn in Budget 2024 and remain absent even after 2026.

Strategic Implications for Different Investor Types

1. Original Subscribers (Primary‑Issue Investors)

If you are an individual who bought SGBs directly from RBI and plan to hold till maturity, the change is largely benign:

- Hold till 8 years: Capital‑gains‑exemption remains intact.

- Avoid premature redemption after 1 April 2026: Early exit will trigger capital‑gains tax instead of the earlier tax‑free benefit.

This group still has the most tax‑efficient structure and can continue treating SGBs as a core gold‑exposure asset.

2. Secondary‑Market SGB Buyers

For those who bought SGBs on the stock exchange, the tax‑free‑maturity rationale no longer holds from 1 April 2026.

- Whether you sell early, redeem prematurely, or hold to maturity, gains will generally be taxed at 12.5% (LTCG) or at slab rates (STCG).

- If your primary reason for buying was expecting tax‑free maturity, you may need to reassess your allocation and compare SGBs with alternatives like Gold ETFs, which are now taxed on a broadly similar basis.

3. Investors Needing Cash Before April 2026

For certain SGB issues, premature‑redemption windows fall before 1 April 2026. For example, specific 2019–20 and 2020–21 series have early‑redemption dates in February–March 2026.

- If you exercise those windows before 1 April 2026, the redemption may still fall under the old, tax‑exempt regime, even if the SGB was bought in the secondary market.

- This is a time‑bound opportunity and should be discussed with your broker or bank, because tax treatment near the cut‑off date is nuanced and fact‑specific.

SGBs vs Other Gold‑Linked Options (Post‑2026)

To help readers decide whether SGBs still fit, a quick comparison helps:

| Aspect | Sovereign Gold Bonds (SGBs) | Gold ETFs / Gold Mutual Funds |

| Underlying exposure | 999‑purity gold, linked to average price over 3 business days. | 24‑karat gold, typically tracked via physical gold reserves. |

| Minimum investment | 2 grams (≈ ₹10k – ₹15k). | 1 unit, often equivalent to 1 gram; can be lower. |

| Maximum limit | 4 kg for individuals/HUFs; 20 kg for trusts (per FY). | No statutory cap. |

| Liquidity | Less liquid; early exit optional only after 5 years, and exchange volumes can be thin. | Highly liquid: can be bought/sold intra‑day on the exchange. |

| Returns | Capital appreciation + 2.5% fixed interest. | Capital appreciation only (no interest). |

| Tax (long‑term) | Maturity‑linked gains exempt only for original‑issue 8‑year individual holders; others face 12.5% LTCG without indexation. | LTCG at 12.5% (no indexation) for qualifying holding periods. |

| Custody costs | No recurring charges. | Expense ratio/brokerage applies. |

This makes SGBs attractive for long‑term, buy‑and‑hold investors who value interest income and capital‑gains tax‑exemption (if eligible), while ETFs suit those who want liquidity and frequent trading.

📊 Stay Ahead in Tax & Accounting

Get the latest updates, circulars, compliance alerts, and expert insights — all in one place.

🚀 Visit TaxRoutine.comBroader Takeaways for Investors

SGBs remain sovereign‑backed and safe, but their tax‑efficiency has shrunk after 2026, especially for secondary‑market buyers and premature redeemers.

The old “tax‑free for everyone” image is gone; the real edge now belongs only to original‑issue, 8‑year‑holding individual investors.

For existing holdings—particularly those acquired on the exchange—reviewing your holding period, exit plans, and tax status (including NRI status) and consulting a tax advisor before 1 April 2026 can help minimise unintended tax outflows.

Should You Invest in SGBs After 2026?

To cap this analysis, consider:

- Stick with SGBs if:

- You are an individual investor.

- You can realistically hold 8 years without liquidity pressure.

- You are subscribing directly at original issue and want tax‑free gold appreciation + 2.5% interest.

- Look elsewhere if:

- You plan to buy on the exchange and exit early, as gains will be taxed and there is no indexation benefit.

- You are sensitive to an 8‑year commitment or prefer highly liquid, daily‑traded gold instruments like ETFs or digital‑gold platforms.

About the Author

Shruthi Keerthi

Executive Editor

Shruthi Keerthi is a Semi-Qualified Chartered Accountant and Company Secretary with 3+ years of diverse experience in Auditing, Taxation, Secretarial Compliances, and Financial Reporting. Her professional journey has been shaped by a strong foundation in finance, complemented by a growing expertise in data analytics. As a Certified Data Analyst, Shruthi specializes in leveraging tools such as Excel, Python, MySQL, Tableau, and Power BI to transform complex data into meaningful business insights. Her work spans across financial performance analysis, KPI monitoring, and building dynamic dashboards that support strategic decision-making. Through article writing, she aims to bridge the gap between traditional finance and modern data-driven practices—sharing insights, practical guides, and real-world experiences that help professionals navigate the evolving landscape of finance, compliance, and analytics.