Input Service Distributor (ISD)

Under GST: The Complete Guide

How the ISD mechanism prevents ITC from being stranded at the head office — registration, distribution rules, GSTR-6, and the 2024 mandatory ISD amendment.

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- Part 2 — Section 16: Conditions for Claiming ITC

- Part 3 — Blocked Credits under Section 17(5)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- Part 6 — ITC Reversal under Rule 37: Practical Difficulties

- ▶ Part 7 — Input Service Distributors (You are here)

📌 At a Glance

- An ISD is an office that receives invoices for common input services used by multiple branches and distributes the ITC to those branches.

- Governed by Section 20 of the CGST Act and Rule 39 of the CGST Rules.

- ISD can distribute ITC on input services only — not on goods or capital goods.

- Distribution is done through an ISD invoice — not a tax invoice — and filed via GSTR-6 (due by 13th of following month) on the GST portal.

- Following the Finance Act 2024 amendment (effective 1 April 2025), ISD registration is now mandatory for entities with common input service invoices across multiple GSTINs.

- ITC distribution ratio is based on the turnover of each recipient unit in the preceding financial year.

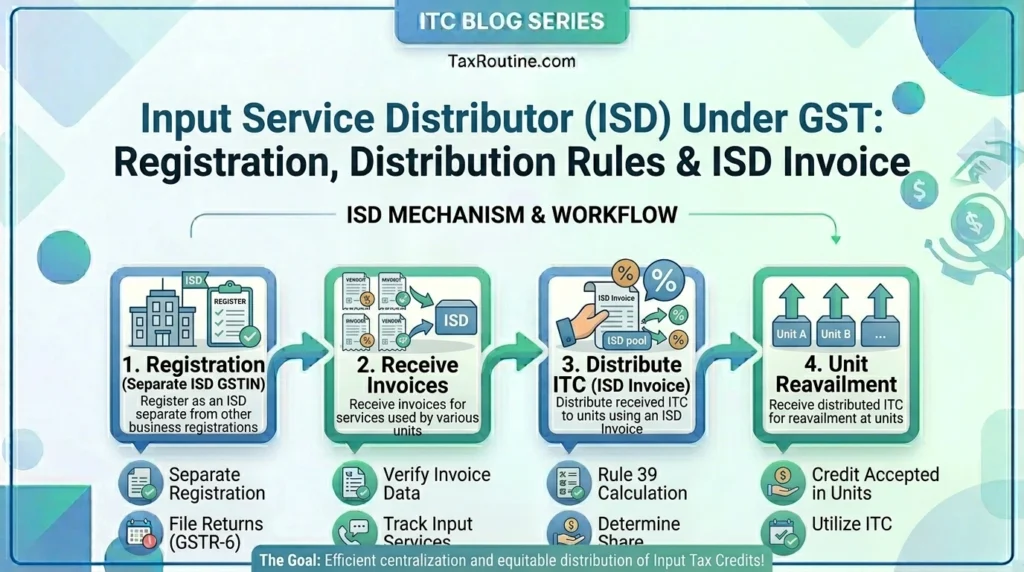

1. What is an Input Service Distributor?

Large businesses with multiple branches across India often receive centralised invoices at their head office — for services like software licences, annual maintenance contracts, audit fees, legal retainers, and advertising. These services benefit all units, but the invoice comes in one unit’s name. Without a distribution mechanism, the ITC on these invoices would accumulate at the head office and could not be transferred to the branches that actually used the services.

The Input Service Distributor (ISD) mechanism solves this by allowing a registered office to receive tax invoices for GST input services and distribute the ITC to recipient units using an ISD invoice, filing a separate return — GSTR-6 — through the GST portal.

2. Statutory Framework: Section 20 & Rule 39

The ISD mechanism is governed by Section 20 of the CGST Act, 2017, which prescribes the conditions for distribution, and Rule 39 of the CGST Rules, which sets out the operational requirements including the ISD invoice format and distribution ratios.

The ITC distributed by an ISD must not exceed the ITC available for distribution. The distribution must be proportionate to the turnover of the recipient units. ITC attributable to a specific unit must go only to that unit. And the ISD must use a prescribed ISD invoice — not a regular tax invoice — to effect the transfer. Read the full text of Section 20 on CBIC.gov.in →

3. What Can & Cannot Be Distributed Through ISD

| Type of ITC | Can ISD Distribute? | Alternative |

|---|---|---|

| Input services (legal, IT, HR, advertising, audit) | Yes — ISD route | — |

| Goods / raw materials | No | Cross Charge or direct invoicing to branch |

| Capital goods | No | Cross Charge or direct invoicing to branch |

| Input services used exclusively by one branch | Yes — full credit to that branch | — |

| Input services used by all branches (common) | Yes — proportionate distribution | — |

| Blocked credits under Section 17(5) | No | Cannot be distributed — ineligible at source |

| ITC on reverse charge services received by ISD | Yes | ISD pays reverse charge and can then distribute the ITC |

4. ITC Distribution: The Turnover-Based Formula

The distribution of ITC by an ISD to its recipient units is done in the ratio of their respective turnovers in the preceding financial year. Rule 39 prescribes three scenarios:

| Scenario | Distribution Rule |

|---|---|

| ITC attributable to a specific unit only | Full ITC goes to that unit — no apportionment |

| ITC attributable to a specific state | Distributed among units in that state proportionate to their turnover ratio |

| ITC attributable to all units (e.g., group audit fees, enterprise software) | Distributed to all units proportionate to each unit’s turnover as a share of total turnover of all units in the preceding FY |

Note: Turnover here means the aggregate turnover of each GSTIN (branch/unit).

A company’s HO receives a ₹10,00,000 + 18% GST enterprise software invoice (total ITC = ₹1,80,000)

The software is used by all three branches. Preceding FY turnovers:

Branch A (Chennai): ₹5,00,00,000 → 50% share

Branch B (Mumbai): ₹3,00,00,000 → 30% share

Branch C (Delhi): ₹2,00,00,000 → 20% share

ITC to Branch A: ₹1,80,000 × 50% = ₹90,000

ITC to Branch B: ₹1,80,000 × 30% = ₹54,000

ITC to Branch C: ₹1,80,000 × 20% = ₹36,000

The ISD issues three separate ISD invoices — one to each branch. Each branch reflects the received ITC in their GSTR-3B as ITC from ISD.

5. The ISD Invoice: Format & Requirements

| Particulars | Regular Tax Invoice | ISD Invoice |

|---|---|---|

| Purpose | Evidence of supply; triggers ITC in buyer’s hands | Transfers ITC from ISD to recipient unit — no new supply |

| GST charged? | Yes — CGST, SGST, or IGST as applicable | No — only the ITC amount is mentioned, no fresh tax |

| Serial number prefix | Business-specific series | Must contain the prefix “ISD” |

| Mandatory particulars | Name, address, GSTIN of supplier and recipient, HSN/SAC, taxable value, tax rate and amount | Name, address, GSTIN of ISD; name, address, GSTIN of recipient unit; original invoice reference; ITC amount being distributed (CGST, SGST, IGST split) |

| Cross-state ITC transfer? | N/A | Yes — IGST credit from ISD can go to any state branch |

| Reflected in recipient’s GSTR-2B? | Yes — from supplier’s GSTR-1 | Yes — auto-populated from ISD’s GSTR-6 on GST portal |

One of the most useful features of the ISD mechanism is that it allows IGST credit to be distributed to branches in any state. If the HO (in Tamil Nadu) receives an invoice with IGST, it can distribute that credit to a branch in Maharashtra. The CGST/SGST credit, however, can only be distributed as IGST to out-of-state branches — it cannot be distributed as CGST or SGST to branches in other states.

6. GSTR-6: The ISD Return

An ISD must file GSTR-6 — a monthly return — containing details of all ITC received and distributed during the month. Filed through the GST portal, GSTR-6 is the mechanism by which the distributed credit flows into the recipient units’ GSTR-2B.

| GSTR-6 Detail | Position |

|---|---|

| Who files | Every registered ISD — through the GST portal |

| Due date | 13th of the following month |

| Frequency | Monthly — no quarterly option for ISD |

| Table 3 | ITC received by ISD (from GSTR-2B — auto-populated) |

| Table 4 | ITC distributed to recipient units (ISD invoices issued) |

| Table 5 | ITC distributed — recipient GSTIN-wise breakup |

| Effect on recipient | ITC distributed in GSTR-6 auto-populates in recipient’s GSTR-2B for the same month |

| Late fee | ₹25 per day (₹10 per day for nil return); maximum ₹5,000 per return |

7. The Finance Act 2024 Amendment: ISD Now Mandatory

Prior to the Finance Act 2024, businesses had a choice between the ISD route and the Cross Charge mechanism. The Finance Act 2024 amendment to Section 20, effective 1 April 2025, has made ISD registration and distribution mandatory for all entities that receive common input service invoices applicable to multiple GSTINs.

If your organisation has multiple GST registrations and receives common input service invoices at a central GSTIN, you must now register that entity as an ISD on the GST portal and start distributing ITC through GSTR-6. Continuing to use Cross Charge for input services without ISD registration may result in ITC being treated as wrongfully distributed — with 24% interest under Section 50(3) and demand under Section 74.

| Parameter | ISD Route | Cross Charge Route |

|---|---|---|

| Applicable to | Input services (mandatory from 1 April 2025) | Goods, capital goods, employee cost allocation (still applicable) |

| GST charged? | No — ITC transferred without fresh GST | Yes — branch raises a taxable supply invoice with GST |

| Registration required? | Yes — separate ISD registration via gst.gov.in | No separate registration — uses existing GSTIN |

| Return filing | GSTR-6 (monthly, by 13th) | Normal GSTR-1 and GSTR-3B of the charging entity |

| Cash flow impact | No fresh GST outflow — only ITC transfer | Fresh GST payable on cross-charge supply |

| Valuation disputes | None — turnover ratio is prescribed | Risk of valuation disputes on cross-charge supply |

8. ISD Compliance Checklist

| Task | Frequency | Action |

|---|---|---|

| Register the distributing office as ISD | One-time | Apply on gst.gov.in — separate GSTIN issued for ISD |

| Update suppliers with the ISD GSTIN | One-time / as needed | Ensure common service invoices are raised in the ISD GSTIN’s name |

| Verify ITC in GSTR-2B of ISD GSTIN | Monthly | Reconcile ISD’s GSTR-2B against invoices received for common services |

| Identify distribution category for each invoice | Monthly | Classify: exclusive to one unit, common to one state, or common to all units |

| Compute distribution amounts using turnover ratio | Monthly | Use preceding FY turnover of each recipient GSTIN; update ratios each April |

| Issue ISD invoices to each recipient GSTIN | Monthly | ISD invoice series with “ISD” prefix; separate invoice per recipient per original invoice |

| File GSTR-6 | Monthly — by 13th | Report ITC received and distribution via GST portal |

| Confirm blocked credits are excluded from distribution | Monthly | ITC blocked under Section 17(5) cannot be distributed — identify and exclude before filing GSTR-6 |

9. Common Mistakes in ISD Implementation

- Distributing more ITC than received: The ISD cannot distribute ITC in excess of what is available in its electronic credit ledger. Excess distribution is treated as wrongful ITC at recipient level — 24% interest under Section 50(3) applies.

- Using turnover ratios of the current year instead of preceding FY: Rule 39 specifies preceding financial year turnover. Using current-year ratios is non-compliant.

- Not issuing ISD invoices for exclusive services: Even if a service benefits only one branch, an ISD invoice must be issued — the ITC cannot sit at the ISD level.

- Distributing blocked ITC: ITC that is blocked at the ISD level under Section 17(5) cannot be distributed to branches.

- Missing the GSTR-6 deadline: Late filing of GSTR-6 means the distributed credit does not appear in recipients’ GSTR-2B for that month — causing cascading compliance issues at the branch level.

- Not registering as ISD after the April 2025 mandatory amendment: Entities that continue to use Cross Charge for input services without ISD registration are now non-compliant and at risk of ITC demands with interest under Section 50.

Frequently Asked Questions

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- Part 2 — Section 16: Conditions for Claiming ITC

- Part 3 — Blocked Credits under Section 17(5)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- Part 6 — ITC Reversal under Rule 37: Practical Difficulties

- ▶ Part 7 — Input Service Distributors (You are here)