Table of Contents

Introduction

Accounting Standard 1 (AS 1) deals with the disclosure of significant accounting policies followed in preparing and presenting financial statements. The objective is to ensure that financial statements provide a true and fair view by disclosing all significant accounting policies that have been adopted.

Applicability

AS 1 is applicable to all enterprises, irrespective of their size or nature of operations. This universal applicability ensures consistency and comparability across financial statements of different entities.

Major Provisions

Principle of Consistency

The principle of consistency is a cornerstone of reliable financial reporting. It mandates that an enterprise applies the same accounting policies and methods from one period to the next. This uniformity ensures comparability, allowing stakeholders—such as investors, auditors, and management—to analyze trends and performance over time without the confusion of shifting standards. AS 1 emphasizes on the principle of consistency to keep the financial statements relevant for its users.

For instance, if a company uses a specific depreciation method one year, switching to another the next without a valid reason could distort its financial picture. Consistency builds trust and clarity, making it easier to spot genuine changes in financial health rather than discrepancies caused by altered approaches.

Principle of Prudence

The principle of prudence emphasizes caution in financial reporting, a safeguard against overly optimistic projections. It requires preparers of financial statements to exercise restraint, ensuring that assets and income are not overstated while liabilities and expenses are not understated. This conservative approach protects stakeholders by presenting a realistic, rather than inflated, view of a company’s financial position.

For example, if there’s uncertainty about collecting a receivable, prudence dictates recognizing a potential loss rather than assuming full recovery. By prioritizing reliability over speculation, this principle helps mitigate risks and fosters confidence in the reported figures.

Principle of Materiality

The principle of materiality focuses on relevance in financial disclosures. It stipulates that all material items—those significant enough to influence the decisions of users—must be fully disclosed in financial statements. What qualifies as “material” depends on context; a small expense might be trivial for a large corporation but critical for a small business.

This principle ensures transparency, enabling users like shareholders or creditors to make informed choices based on impactful data. The Ministry of Corporate Affairs underscores its importance, highlighting that omitting or misstating material facts could mislead stakeholders, undermining the integrity of financial reporting.

Why These Principles Matter

Together, consistency, prudence, and materiality form the bedrock of credible accounting. Consistency provides a stable framework for comparison, prudence guards against overconfidence, and materiality ensures that key details aren’t overlooked.

These principles align financial reporting with the needs of its users, balancing accuracy and practicality. For enterprises, adhering to them isn’t just a regulatory obligation—it’s a commitment to transparency and accountability, fostering trust in an increasingly complex economic landscape.

Disclosure Requirements

AS 1 mandates that all significant accounting policies adopted in the preparation and presentation of financial statements should be disclosed. These disclosures should form part of the financial statements and be presented in one place to facilitate understanding. If there has been a change in any accounting policy that has a material effect on the financial statements, the nature of such change and its effect should be disclosed. If the effect of such change is not ascertainable, the fact should be indicated.

Examples

- Depreciation: If a company adopts the straight-line method of depreciation for its fixed assets, this policy should be disclosed in the financial statements.

- Valuation of Inventories: If inventories are valued at the lower of cost and net realizable value, this accounting policy should be explicitly stated.

- Revenue Recognition: The basis on which revenue is recognized (e.g., upon delivery of goods, completion of services) should be disclosed.

Importance of AS 1

The disclosure of accounting policies is crucial as it aids users of financial statements in understanding how accounting principles have been applied. This understanding enhances the comparability of financial statements between different enterprises and across different periods. Transparent disclosure of accounting policies also promotes better corporate governance and builds investor confidence.

Conclusion

Accounting Standard 1 emphasizes the importance of disclosing significant accounting policies to ensure that financial statements present a true and fair view. By adhering to the principles of consistency, prudence, substance over form, and materiality, and by transparently disclosing accounting policies, enterprises can enhance the reliability and comparability of their financial statements.

For More information of the Accounting Standard and to access the bare text of the standard visit ICAI’s official website

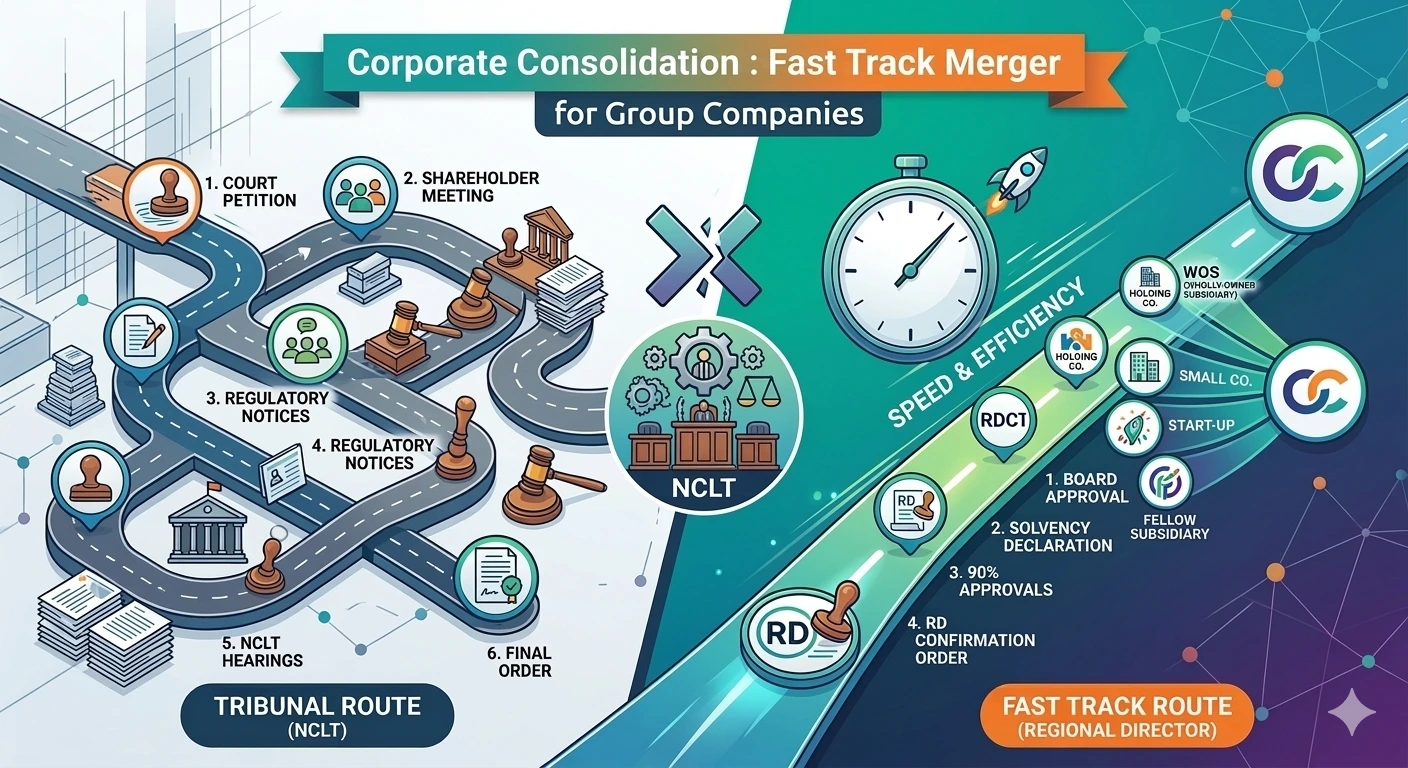

Tax Implications of Fast-Track Mergers in India

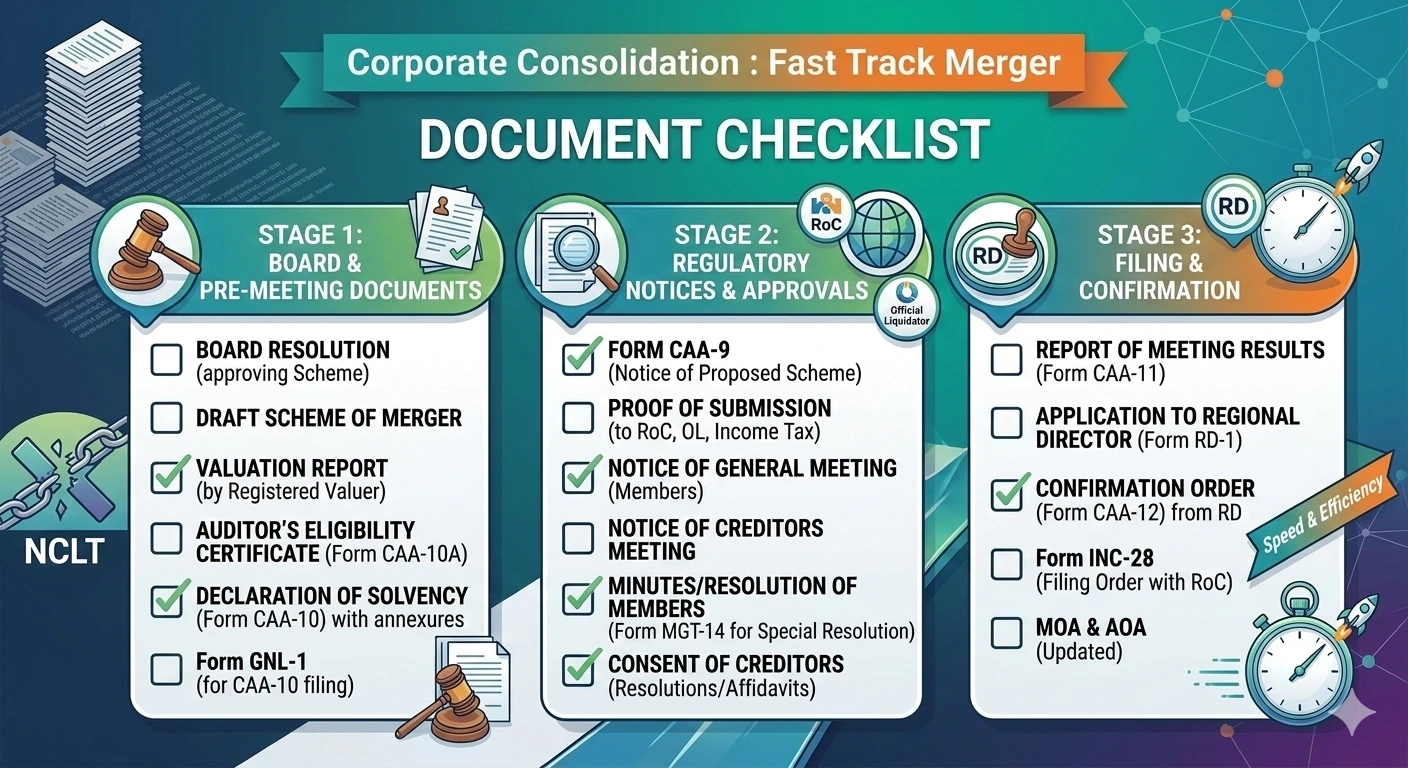

Fast-Track Merger Document Checklist (Section 233 – Practitioner Guide)