Vivad Se Vishwas Scheme 2024

The Direct Tax Vivad Se Vishwas Scheme, 2024 (hereinafter referred as DTVSV Scheme,2024) has been enacted vide Chapter IV of Finance (No.2) Act, 2024 to provide for dispute resolution in respect of pending income tax litigation. The objective of the Scheme is to, inter alia, reduce pending income tax litigation, generate timely revenue for the Government and benefit taxpayers by providing them peace of mind, certainty and savings on account of time and resources that would otherwise be spent on the long-drawn and vexatious litigation process.

This scheme was notified by the Government of India on September 20, 2024 to resolve the pending appeals in the case of Income Tax and the scheme was made effective from 1st October 2024.

When DTVSV scheme was notified by the Government they had introduced four forms namely:

- Form-1 : Form for filing declaration and commitment by the declarant

- Form-2: Form for certificate to be issued by the Designated Authority

- Form-3 : Form for intimation of payment by the declarant

- Form-4 : Order for full and final settlement of tax arrears by the Designated Authority

The Taxpayers are required to determine the amount payable under the Vivad Se Vishwas Scheme in Form-2 and make the intimation of payment made to The Designated Authority in Form-3.

As per this scheme the taxpayers and the Department can clear of their outstanding appeals before various appellate authorities of the Income Tax.

Amount Payable under DTVSV

As per Section 90 of the Finance (No. 2) Act 2024, the declarant is required to determine the amount payable under DTVSV scheme.

| Nature of Tax Arrear | Amount Payable under this scheme till 31st January 2025 | Amount Payable under this scheme after 31st January 2025(i.e from 1st February 2025) |

Where the tax arrear is the aggregate amount of disputed tax, interest chargeable or charged on such disputed tax and penalty leviable or levied on such disputed tax in a case where the declarant is an appellant after the 31st day of January, 2020 but on or before the specified date. | Amount of the disputed tax. | The aggregate of the amount of disputed tax and ten per cent of disputed tax. |

| Where the tax arrear is the aggregate amount of disputed tax, interest chargeable or charged on such disputed tax and penalty leviable or levied on such disputed tax in a case where the declarant is an appellant on or before the 31st day of January, 2020 at the same appellate forum in respect of the such tax arrear. | The aggregate of the amount of disputed tax and ten per cent of disputed tax. | The aggregate of the amount of disputed tax and twenty per cent of disputed tax |

Where the tax arrear relates to disputed interest or disputed penalty or disputed fee where the declarant is an appellant after the 31st day of January, 2020 but on or before the specified date. | Twenty-five per cent of disputed interest or disputed penalty or disputed fee. | Thirty per cent of disputed interest or disputed penalty or disputed fee. |

Where the tax arrear relates to disputed interest or disputed penalty or disputed fee where the declarant is an appellant on or before the 31st day of January, 2020 at the same appellate forum in respect of the such tax arrear. | Thirty per cent of disputed interest or disputed penalty or disputed fee. | Thirty-five per cent of disputed interest or disputed penalty or disputed fee. |

This notification is issued in exercise of powers conferred under clause (l) of sub-section (1) of section 89 of the Finance (No. 2) Act, 2024. As per this notification issued by the Ministry of Finance on 8th April 2025 has issued the Due date as 30th April 2025 for declaration in respect of tax arear filed by the declarant to the designated authority in accordance with Section 90 of the said act.

Vivad-se-viswasAlso See

Tax Implications of Fast-Track Mergers in India

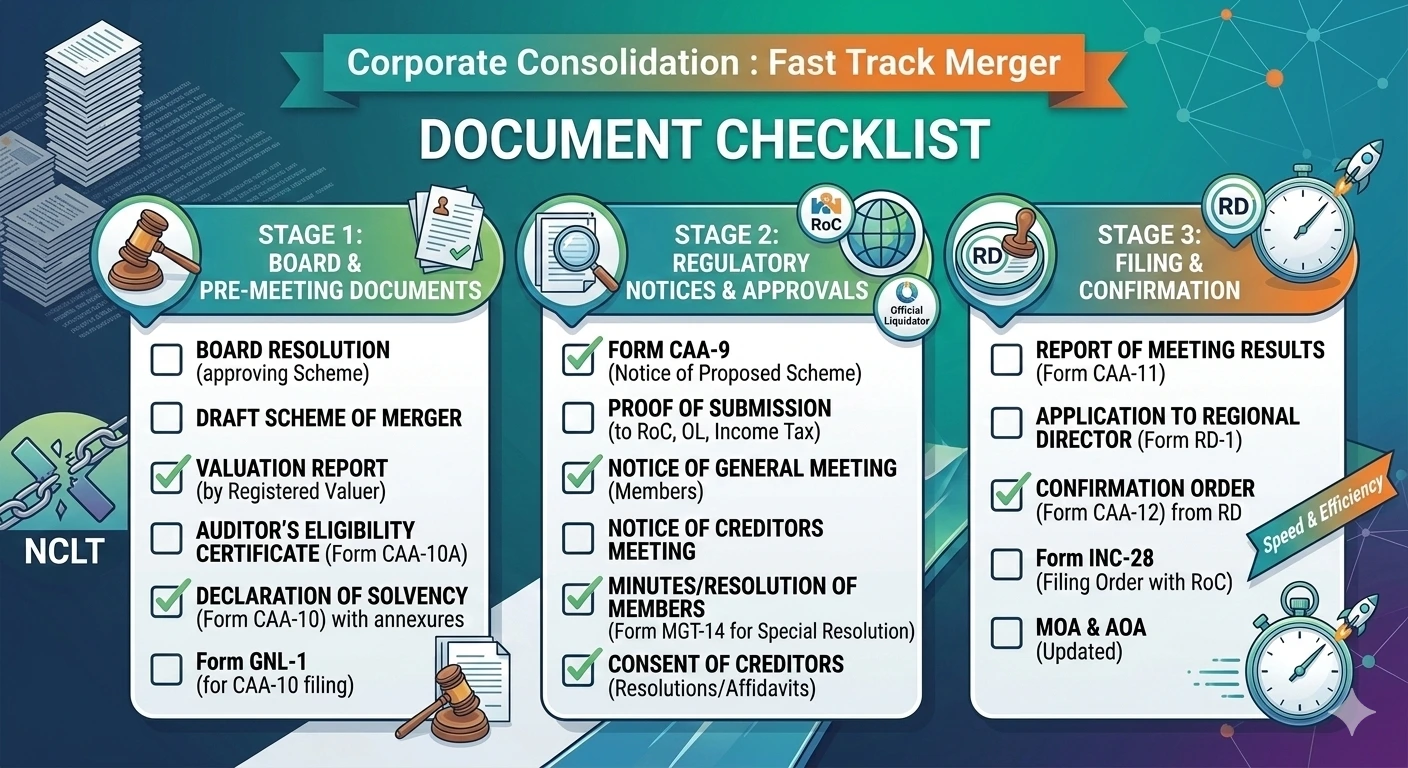

Fast-Track Merger Document Checklist (Section 233 – Practitioner Guide)

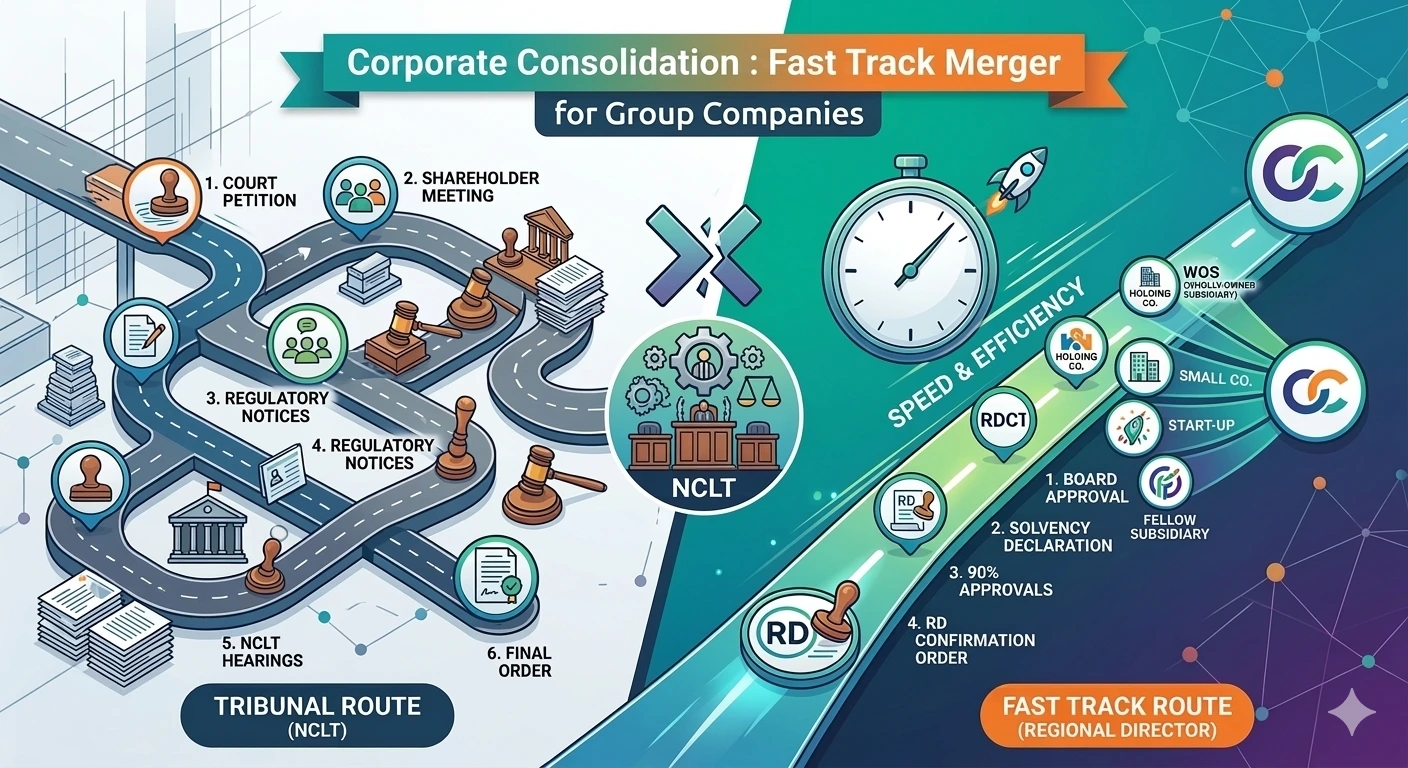

Streamlining Corporate Consolidation: A Guide to Fast Track Mergers for Group Companies

Compliance Calendar March 2026

GST Cash Ledger vs. Income Tax “Cash Ledger”: Concept and Challenges