Form No. 145 (Erstwhile Form 15CA): Everything You Need to Know Before Making a Foreign Remittance

📋 Quick Reference

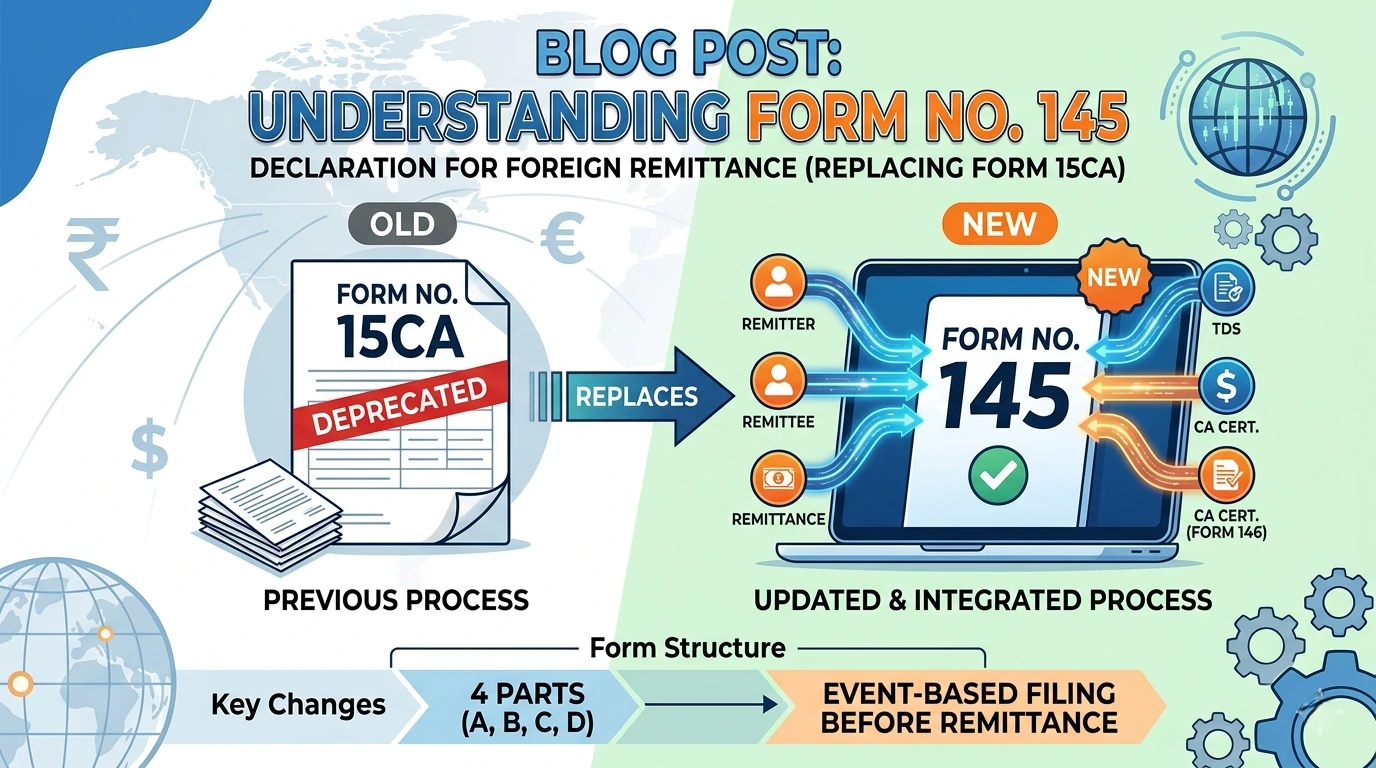

1What is Form No. 145?

Form No. 145 is a mandatory declaration that must be filed by any person or entity intending to remit funds to a non-resident (not being a company) or a foreign company. It must be submitted before the payment is made.

It serves three key purposes: it reports foreign remittances chargeable to tax in India, ensures proper TDS deduction under Section 393(2), and helps the Income Tax Department track cross-border payments through ITBA integration for risk profiling and verification.

2Who Must File — and Who Is Exempt?

Every person responsible for paying a non-resident or foreign company must file Form No. 145 under Rule 220 before remitting. However, three categories are exempt:

- Remittances by an individual that do not require prior RBI approval — i.e., payments under the Liberalised Remittance Scheme (LRS)

- Remittances made by a unit of an International Financial Services Centre (IFSC)

- Remittances of the nature specified under the relevant RBI purpose code

3Which Part of the Form Applies to You?

Form No. 145 has four parts. Your choice depends on the taxability of the remittance and its amount:

| Part | When to Use |

|---|---|

| Part A | Remittance is taxable and the amount (or aggregate for the year) does not exceed ₹5 lakh |

| Part B | Remittance is taxable, exceeds ₹5 lakh, and you hold an AO certificate u/s 395(1)/(2) |

| Part C | Remittance is taxable, exceeds ₹5 lakh, and you have a CA certificate in Form No. 146 (no AO certificate) |

| Part D | Remittance is not chargeable to tax in India |

4Documents Required

- Invoice, agreement, or contract related to the foreign remittance

- Details of remitter, remittee, remittance amount, and bank details

- AO certificate u/s 395(1)/(2) — only for Part B

- CA certificate in Form No. 146 — only for Part C

- Form No. 41 and Tax Residency Certificate (TRC) of the remittee — only if claiming DTAA benefits

- TIN (Tax Identification Number) of remittee if they do not have Indian PAN

5How to File Form No. 145

You can file online or offline (bulk). Here is the online process:

6After Filing: Modification & Withdrawal

- Modification: Not allowed. Once submitted, Form No. 145 cannot be edited or modified.

- Withdrawal: Allowed within 7 days of the submission date.

- Linked Form No. 146: If you withdraw Part C of Form No. 145, the linked Form No. 146 (CA’s certificate) is automatically updated to “Withdrawn” status.

7Penalty for Non-Compliance

Up to ₹1 Lakh Penalty

Under Section 462 of the Income-tax Act, 2025, failure to file Form No. 145 or providing inaccurate information attracts a penalty of up to ₹1,00,000.

8Key Changes from Form 15CA to Form No. 145

Physical copy submission to bank (AD) mandatory

Aadhaar details required for remitter and remittee

No TIN field for remittee without PAN

AO certificate details present in Part C

No UDIN requirement for CA certificate

No ITDREIN field

✅ Electronic delivery to bank now permitted

✅ Aadhaar details removed

✅ TIN field added for non-PAN remittees

✅ AO certificate removed from Part C (use Part B instead)

✅ UDIN mandatory for Form No. 146 (CA certificate)

✅ ITDREIN field added for cross-verification with Form No. 147

Download Form No. 145

Access the official CBDT form in PDF and Word (.docx) formats directly.

Detailed Article on Form No. 145

Access a detailed article with expanded definitions, FAQs and even more information.