Table of Contents

Introduction

The Goods and Services Tax (GST) has significantly transformed India’s indirect tax structure by unifying various taxes under a single regime. Under the GST law, an unregistered person cannot collect tax from customers nor claim Input Tax Credit (ITC) for the taxes paid on purchases.

Registration under GST is essential as it legally recognizes a person as a supplier of goods or services—or both—and authorizes them to:

- Collect tax on outward supplies,

- Remit the collected tax to the Government, and

- Pass on the credit of input taxes to recipients.

In this blog, we’ll explore who is required to register under GST, the turnover thresholds, exceptions, and special cases where registration is compulsory.

Who is a Taxable Person?

As per section 2(107) of the CGST Act 2017, Taxable Person means a person who is registered or liable to be registered under section 22 or section 24;

The following persons are also called as Taxable persons:

- An unregistered person who is liable to be registered

- A person not liable to be registered under GST but has taken voluntary registration and has got himself registered under GST.

The term person includes:

- Individual

- Hindu Undivided Family (HUF)

- Company

- Firm

- Limited Liability Partnership (LLP)

- Association of Persons (AOP) or Body of Individuals (BOI)

- Local authority

- Trusts or societies

- Any government body or corporation

Who is liable to be registered under GST?

Persons liable for registration [Section 22]

As per section 22 of the GST Act any person who is engaged in the supply of goods or services or both is required to registered under the GST Act if the aggregate turnover exceeds the specified limit in a financial year.

The following persons are required to be registered under GST:

- Every supplier whose aggregate turnover exceeds the specified limit as stated above.

- Every person who has already been registered under the previous laws (i.e like VAT, service Tax etc)

- If a business which is being carried on by a taxable person is transferred or on account of succession to another person on a going concern basis, the transferee or the successor is required to take a new GST registration.

- In case of an arrangement for amalgamation or in case of a de-merger the transferee is required to be registered under GST from the date the ROC issues the certificate of incorporation.

“Key Terms”:

Aggregate Turnover – means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both and inter-State supplies of persons having the same Permanent Account Number, to be computed on all India basis but excludes central tax, State tax, Union territory tax, integrated tax and cess;

| Includes the following | Excludes the following |

|---|---|

| •Total turnover of all branches (i.e all GST registrations under same PAN) | •Inward supplies on which tax is payable on reverse charge basis |

| •Value of exported goods/services, exempted goods/services, inter-state supplies including inter-state supplies between distinct persons having same PAN | •Elements of Tax i.e CGST, SGST/UTGST, IGST and compensation cess |

| •All supplies made by the taxable person whether for him or on behalf of his principals. | •Value of goods, after completion of Job work supplied directly from the premises of the Job worker not to be included in the turnover of the Job worker. |

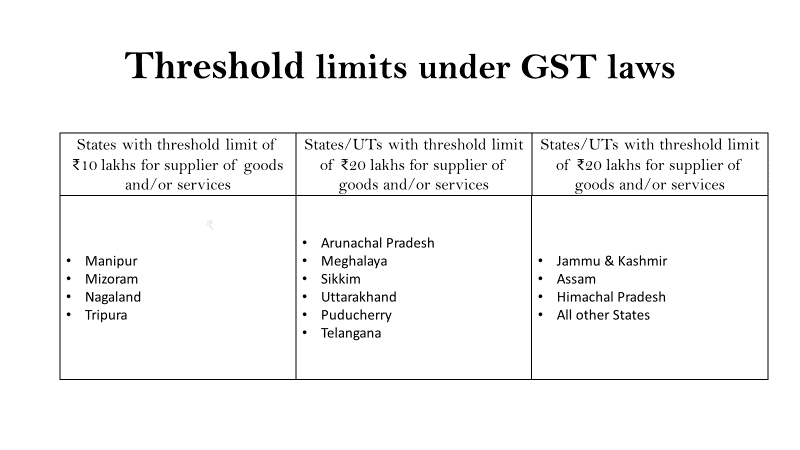

Special Category States – The following states are considered as special category states namely Mizoram, Manipur, Nagaland, Tripura, and others, except J&K, Arunachal Pradesh, Assam, Himachal Pradesh, Meghalaya, Sikkim, and Uttarakhand

Further Notification No. 10/2019 CT dt 07-03-2019 exempts any person who is engaged exclusively in supply of goods and whose aggregate turnover in a financial year does not exceed ₹ 40 lakh, from the requirement to obtain a registration.

Exceptions to this exemptions are:

- Persons required to take compulsory registration under section 24;

- Persons engaged in making supplies of

- ice cream & other edible ice, whether or not containing cocoa

- Pan Masala

- Tobacco & manufactured tobacco

- fly ash bricks; fly ash aggregates; fly ash blocks

- Bricks of fossil meals or similar siliceous earths

- Building bricks

- earther or roofing tiles

- Persons engaged in making intra-State supplies in the States of Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Puducherry, Sikkim, Telangana, Tripura, Uttarakhand; and

- Persons who have opted for voluntary registration or such registered persons who intend to continue with their registration under CGST Act.

Compulsory registration in certain cases [Section 24]

While section 22 of the Act states that registration based on threshold limits while section 24 states that in which situations GST registration has to be obtained mandatorily.

The category of persons who are required to mandatorily obtain GST registration are:

| Sl. No. | Category of Person | Explanation |

|---|---|---|

| 1 | Inter-State supplier of taxable goods | E.g., someone in Tamil Nadu supplying goods to Kerala |

| 2 | Casual taxable person | Supplies goods/services occasionally with no fixed place of business |

| 3 | Taxpayer under reverse charge | Tax is required to be paid by recipient on behalf of supplier |

| 4 | Non-resident taxable person | Foreign entities supplying in India |

| 5 | E-commerce operator | Platforms like Amazon, Flipkart, Zomato |

| 6 | Persons supplying through e-commerce operators | E.g., a seller using Amazon to deliver products |

| 7 | TDS deductors under Section 51 | Government departments, PSUs, etc. |

| 8 | Persons making taxable supply of goods or services or both on behalf of other taxable person as an agent | Like commission agents or brokers |

| 9 | Input Service Distributors (ISDs) | Businesses distributing input service credits across branches |

| 10 | Persons required to collect TCS under Section 52 | E-commerce operators collecting tax at source |

| 11 | Persons supplying OIDAR services from outside India to unregistered persons in India | E.g., Netflix, Spotify |

Persons not liable for registration [Section 23]

Section 22 and Section 24 of the Act states that who are all required to apply for GST registration, Section 23 of the Act provides a list of persons who are not required to obtain the registration.

This can be divided into two categories as follows:

Persons not liable to registration

Specified category of persons notified by the Government exempted from obtaining registration

Persons not liable to registration

The following persons are not liable to be registered. Therefore the following persons will not be considered as taxable person.

Persons exclusively engaged in the supply of goods and/or services

A person who is exclusively engaged in the supply of goods and/or services that are wholly exempt from GST are not required to obtain registration.

An Agriculturist to the extent of supply produced from the cultivation of land

A farmer who is involved in the cultivation and selling from their own produce are not required to obtain registration.

Specified category of persons notified by the Government exempted from obtaining registration

The Government may on the recommendations of the council, by way of notification subject to conditions and restrictions may specify the category of persons who are exempted from obtaining GST registration.

The following category of persons have been notified by the Council:

Persons making only reverse charge supplies

As per Notification No. 5/2017 – Central Tax, dated 19.06.2017, the persons who are exclusively engaged in making reverse charge supplies are exempted from obtaining GST registration.

Persons making inter-state supplies of taxable services upto ₹20 lakhs

As per Notification No. 10/2017 – Integrated Tax, dated 13.10.2017 ,persons making inter-state supplies of taxable services and whose aggregate turnover does not exceed ₹20 lakhs in a financial year (₹10 lakhs for special category states) are exempted from obtaining GST registration.

Persons making inter-state supplies of taxable services of notified handicraft goods and notified handmade goods upto ₹20 lakhs

Persons making inter-state supply of the following items are exempted from obtaining registration

- Notified Handicraft Goods

- Notified products when made by craftsmen predominantly by hand even though some machinery is used.

Conditions to be fulfilled:

- Aggregate value of supplies to be computed on all India basis does not exceed ₹20 lakhs (₹10 lakhs in case of special category states) and

- They have obtained a PAN and E-way bill has been generated.

Casual Taxable Persons (CTPs) making inter-state supplies of taxable services of notified handicraft goods and notified handmade goods upto ₹20 lakhs

A CTP is liable to be registered compulsorily under GST irrespective of the threshold limit.

However the following categories of CTPs making inter-state supply of the following items are exempted from obtaining registration

- Notified Handicraft Goods

- Notified products when made by craftsmen predominantly by hand even though some machinery is used.

Conditions to be fulfilled:

- Aggregate value of supplies to be computed on all India basis does not exceed ₹20 lakhs (₹10 lakhs in case of special category states) and

- They have obtained a PAN and E-way bill has been generated.

Persons making supplies of services through E-commerce (other than supplies specified in sec 9(5) )with turnover upto ₹20 lakhs

As per Notification No. 65/2017 – Central Tax, dated 15.11.2017 service providers making supplies through e-commerce operators are exempt from compulsory registration, if:

- Aggregate value of supplies to be computed on all India basis does not exceed ₹20 lakhs (₹10 lakhs in case of special category states) and

- They are not required to register under any other section

Persons making intra-state supplies of goods through ECO with aggregate turnover upto the threshold limit

As per Notification No. 34/2023 – Central Tax, dated 31.07.2023 persons meeting the below mentioned conditions are exempted from obtaining registration even though they supply goods through E-commerce operators.

| Criteria | Requirement |

|---|---|

| Nature of Supply | Intra-State supply of goods only |

| Channel | Supply made through an e-commerce operator (like Amazon, Flipkart, etc.) |

| Turnover | Does not exceed the applicable threshold limit (₹40 lakhs for goods, ₹20 lakhs/₹10 lakhs for special category states) |

| Location | Supplier must be located in a state/UT that has opted in for this exemption (almost all major states have) |

| Exclusion | Supplier must not be making inter-State supply of goods |

Voluntary Registration

Every person even if his turnover does not exceed the threshold limit as stated above can obtain voluntary registration.

Benefits of obtaining voluntary registration:

- It enables the person to issue tax invoices and collect taxes

- It enables him to claim eligible input tax credits (ITC)

- Helps to build credibility of the business

- It helps to avoid future penalties.

Once the registration is obtained it is mandatory to file the GST returns either on monthly / quarterly basis, pay taxes on time and is required to maintain proper books of accounts.

Consequences of non-registration

Whether the liability for registration arises and the person does not obtain the registration certificate on time the following consequences may be faced by the person:

- Will not be able to collect taxes, issue tax invoice and claim eligible input taxes.

- Tax liability on past turnover may be imposed by the authorities if they have found that applicability of registration has arisen already.

- Penalties and Interest may also be imposed for non-registration.

Penalties & Interest are as follows:

| Type | Amount |

|---|---|

| Penalty for non-registration | ₹10,000 or amount of tax evaded, whichever is higher |

| Interest on unpaid tax | 18% per annum (from the due date till actual payment) |

| Penalty for unauthorised collection | Equivalent to the amount collected without GSTIN |

Conclusion

Understanding the GST law is essential for every person engaged in business to ensure timely compliance with the provisions of the Act -relating to the registration process. Regularly reviewing your turnover and business activity helps you determine whether you are liable to register under GST or qualify for any exemptions.

Failing to register when the liability to register arises can lead to interest, penalties, and denial of input tax credit, impacting your overall business. Therefore, it is important to monitor threshold limits regularly and initiate the registration process as soon as the liability arises, to ensure the smooth flow of the business and to have timely compliance of the GST laws.

GST Portal

🔗 Suggested Posts:

Unveiling the process of GST refund

A deep analysis of Invoice Management System

New Instructions regarding processing of applications for GST Registration