In a pivotal moment for India’s fiscal framework, her excellency, The President, Smt. Droupadi Murmu granted her assent to the Income Tax Bill (No.2) 2025 on August 21, 2025, transforming the bill into the Income Tax Act 2025. This legislation, set to replace the venerable but cumbersome Income Tax Act of 1961 from April 1, 2026 (F.Y. 2026-27 onwards), promises a streamlined, modernized approach to taxation without altering core elements like tax rates or penalties.

For millions of Indian taxpayers—ranging from salaried employees navigating deductions to businesses grappling with compliance—this development signals relief from archaic jargon and redundancies that have plagued the system for decades. But the story doesn’t end with the assent. The new Act empowers the Central Government and the Central Board of Direct Taxes (CBDT) to draft and notify fresh rules and schemes, particularly for faceless, tech-driven processes.

This could usher in an era of digital efficiency, reducing human intervention and boosting transparency. In this comprehensive guide, we’ll explore the bill’s journey, key features, major changes, the upcoming rulemaking process, and its potential impacts. Whether you’re a freelancer eyeing simpler filings or an investor concerned about capital gains, understanding these shifts is crucial for staying ahead in the evolving tax landscape.

Journey to President’s Assent

The Income Tax Bill (No.2) 2025 was introduced in the Lok Sabha on August 11, 2025, following the withdrawal of an earlier draft to incorporate insights from a Select Committee. This revised version aimed to address concerns about clarity and practicality, reflecting a collaborative legislative effort. Remarkably, the bill cleared the Lok Sabha in a mere three minutes and sailed through the Rajya Sabha shortly after, underscoring broad parliamentary consensus on the need for reform.

With the President’s Assent, the bill officially becomes law, but its full implementation is deferred to the next financial year, allowing time for transitions and the drafting of supporting rules. Running parallel is the Taxation Laws (Amendment) Bill 2025, which also received assent and introduces immediate adjustments, such as enhanced deductions, effective from the 2024-25 assessment year. This dual approach ensures continuity while paving the way for long-term improvements.

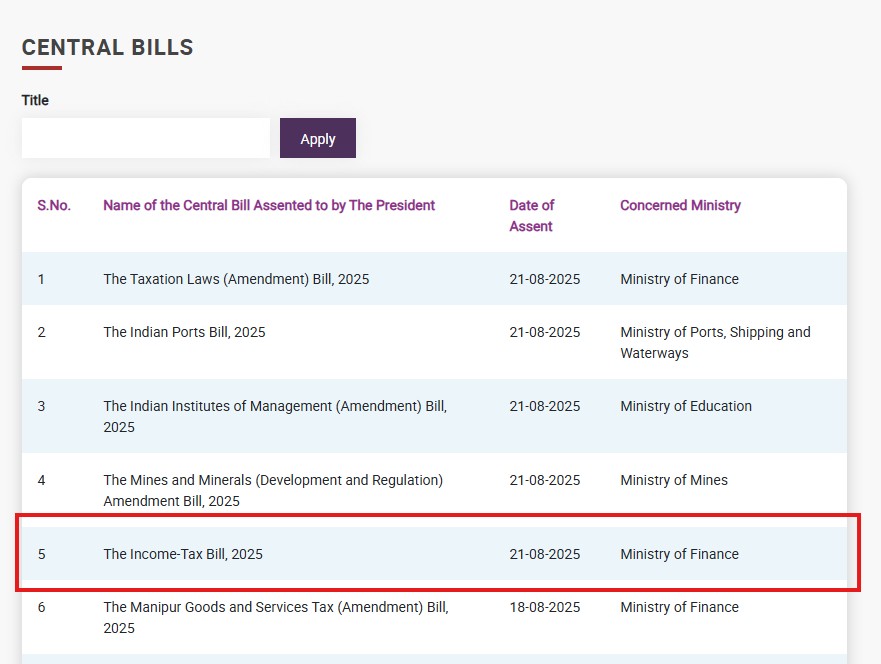

Though the President’s Assent has not been conveyed through media outlets or through official government handles of the Ministry of Finance or the Central Board of Direct Taxes, the President’s Secretariat has posted the list of assented bills under the Central Bills section in its official website – Bills Assented By the President

Income Tax Act 2025 : Core Objective – Simplification at the Heart

President’s Assent to Income Tax Bill (No.2) 2025, now the Income Tax Act (2025), represents a significant milestone in tax legislation. The streamlined framework, aimed at simplification, is poised to enhance operational efficiency within the tax system while upholding core principles.

Key goals include:

- User-Friendly Language: Terms like “previous year” and “assessment year” are unified into “tax year,” and amounts are expressed numerically (e.g., Rs. 2,00,000) for ease.

- Efficiency Boost: By empowering digital tools and faceless interactions, the Act aims to minimize disputes and enhance compliance.

- Transparency and Accountability: Provisions ensure processes are fair, with schemes designed to optimize resources through technology.

This isn’t about increasing tax burdens but making the system more accessible, potentially reducing litigation costs for taxpayers and the government alike.

What’s Changing in the Income Tax Act (2025)?

While the bill preserves the essence of the 1961 Act, it introduces targeted updates to align with contemporary needs. Here’s a deeper dive into the standout changes:

Digital Enforcement and Access Powers

Income tax authorities can now access “virtual digital spaces” during searches, including email servers, social media, and online investment accounts, even overriding access codes if necessary. This expansion acknowledges the digital economy’s role in income generation, ensuring hidden assets in virtual realms aren’t overlooked.

Tax Treaty Interpretations and Clarity

For double taxation avoidance agreements, undefined terms will draw meanings from central laws if not specified in the treaty or notifications. This reduces ambiguities, benefiting cross-border investors and non-residents.

🔗You may also be interested in : DTAA Explained – A Comprehensive Guide to Avoiding Double Taxation u/s 90&91

Dispute Resolution Enhancements

The Dispute Resolution Panel, applicable to transfer pricing and non-resident cases, must now provide reasoned directions, fostering better decision-making and fewer appeals.

Deductions, Exemptions, and Reliefs

- Standard Deduction Hike: Under the new regime, salaried individuals can claim up to Rs. 75,000 for FY 2025-26.

- Pension Parity: The Unified Pension Scheme mirrors New Pension Scheme benefits, with 60% lump-sum withdrawals tax-exempt.

- Infrastructure Incentives: Exemptions extended for Saudi Public Investment Fund investments until March 2030.

- Capital Gains and Property Tweaks: Clarifications on depreciable assets and a post-property-tax 30% deduction for house income.

- TDS/TCS Adjustments: Exemptions for education loan remittances and clearer thresholds for goods purchases.

These modifications, some retroactive, aim to plug gaps and offer taxpayer relief.

New Rules and Schemes: The Drafting Process Ahead

A cornerstone of the Income Tax Act (2025) is its delegation of rulemaking powers to the Central Government and CBDT, enabling agile adaptations without frequent parliamentary amendments. Unlike the 1961 Act’s rigid faceless provisions, the new law grants broad authority to notify schemes for various processes, emphasizing technology-driven, interface-free operations.

Key Areas for New Rules and Schemes

- Faceless Processes: Schemes can be framed for collecting information, conducting assessments, inquiries, valuations, revising orders, and recovering taxes. These must promote efficiency through economies of scale, functional specialization, and minimal human interaction.

- Dispute Resolution and Treaties: Notifications for interpreting treaty terms and detailed guidelines for panels.

- Other Notifications: Potential rules for virtual digital access protocols, MSME alignments, and emerging issues like crypto taxation.

All such schemes require laying before Parliament, ensuring oversight.

How the Drafting Process May Unfold

The CBDT, under the Ministry of Finance, spearheads rulemaking for direct taxes in India. The process typically begins with internal drafting by experts, drawing on stakeholder feedback, economic data, and global best practices. For significant changes—like the faceless schemes—drafts are often released publicly for comments, as seen with the original Income Tax Bill where inputs were solicited via an OTP-verified portal on the e-filing website.

Stakeholders, including tax professionals, industry bodies, and citizens, can submit suggestions within a stipulated period (usually 30-60 days). The CBDT reviews these, incorporates viable ideas, and refines the draft. Once finalized, rules or schemes are notified in the Official Gazette, gaining legal force. In some cases, like presumptive taxation or reporting norms, drafts are explicitly shared for broader consultation.

Given the Act’s April 2026 rollout, expect CBDT to initiate drafting soon, possibly inviting inputs by late 2025. This participatory approach, while not mandatory for all rules, enhances legitimacy and practicality. However, critics note that not all notifications involve public consultation, potentially leading to hurried implementations.

Conclusion: Navigating the Transition

As India gears up for 2026, watch for CBDT notifications on schemes—these will define the Act’s real-world efficacy. The drafting process, blending expertise with public input, could set precedents for future reforms. Taxpayers should monitor the Income Tax Department’s portal for updates and consult experts to adapt. This assent isn’t just a legislative milestone; it’s a step toward a fairer, tech-savvy tax system. What do you think—will these changes ease your tax woes? Share below and subscribe for more insights.

Unlock the New Tax Era with Confidence!

The Income Tax Act 2025 is here—simpler rules, bigger deductions, and digital ease! Don’t navigate alone. Our expert tax advisors will help you save more, stay compliant, and master the changes.

- Custom advice for salaried, freelancers, & businesses

- Stay clear of unwanted Notices!

- Stay ahead of faceless assessments & new rules