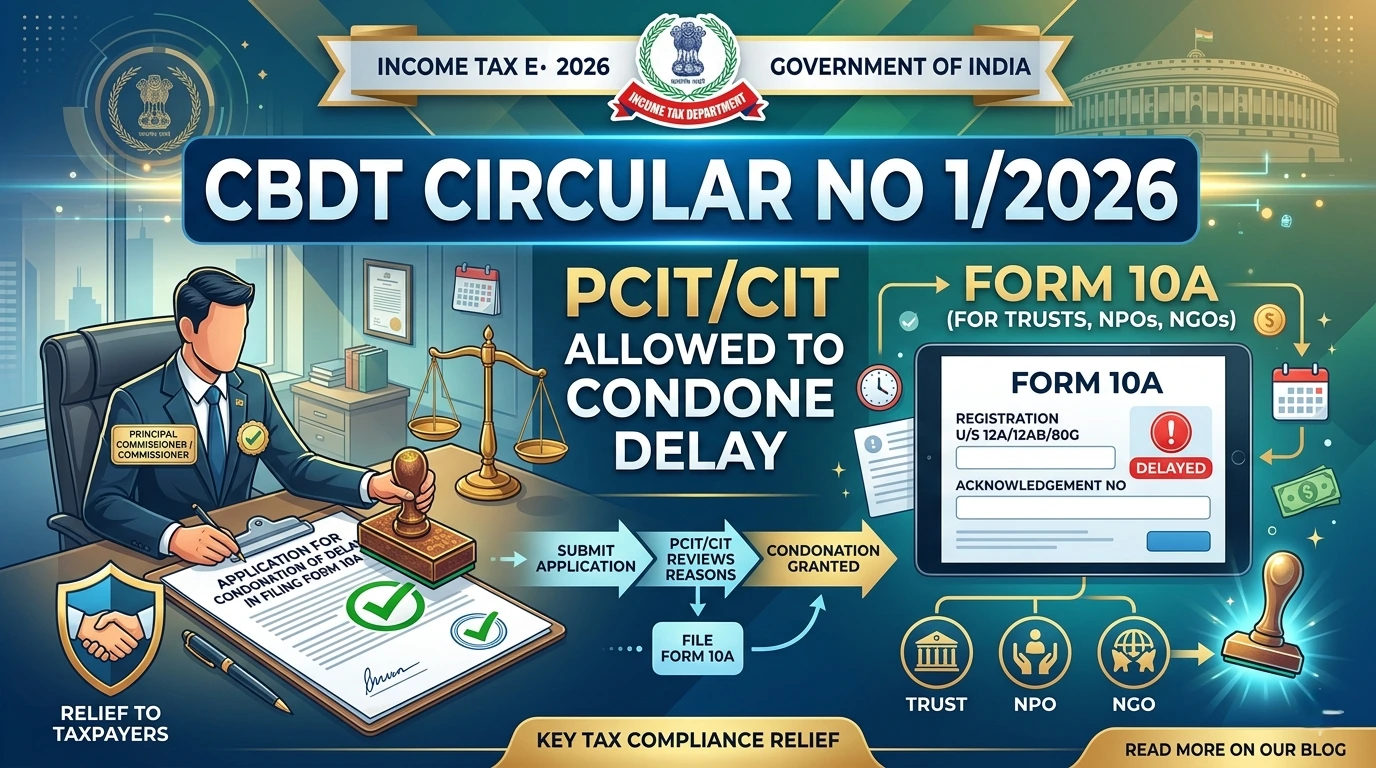

The Central Board of Direct Taxes (CBDT) has finally cleared the long-standing confusion that was causing genuine hardship to thousands of trusts across India. Who can condone delay in Filing Form 10A? was a question that was baffling the trusts as well as the tax professionals alike, because a corresponding amendment to the rules was not made when the governing section was amended. CBDT vide Circular No. 1/2026 dt 23 March 2026 had given certain long awaited clarifications.

What does the Circular No. 1/2026 Say?

Issue before the Circular : With effect from 1 October 2024, a new proviso was added to Section 12A(1)(ac) giving power to the Principal Commissioner of Income Tax or Commissioner of Income Tax to condone delay in filing Form 10A if there is “reasonable cause”.

However, because Form 10A registration is processed only by the Director of Income-tax (CPC), Bengaluru, many Assessing Officers and taxpayers were confused: “Who exactly can condone the delay? The local PCIT/CIT or the CPC Bengaluru?”

CBDT’s Clear Answer (Circular No. 1/2026)

“The jurisdictional Principal Commissioner of Income-tax or Commissioner of Income-tax shall have powers to condone delay in filing Form No. 10A under sub-clause (i) of clause (ac) of sub-section (1) of section 12A.”

This clarification has been issued under Section 119(2)(b) of the Income tax Act to avoid genuine hardship to eligible trusts.

Application for Condonation of Delay

The Principal Commissioner of Income-tax,

PCIT-3, Chennai

👆 Realistic Preview • Exactly how the downloaded file looks

📥 INSTANT DOWNLOAD

Ready-to-Use Form 10A Condonation Application

✅ As per CBDT Circular No. 01/2026

✅ Fully formatted • Letterhead ready • With all enclosures list

✅ One-click replace your details

Direct secure download from taxroutine.com • No signup • Virus-free • Updated 24 Mar 2026

Who Benefits & From When?

- All trusts/institutions whose Form 10A was filed late

- Applications for condonation that are already pending

- Fresh condonation requests filed on or after the date of this Circular

✅ Good news: Even if your Form 10A is already with CPC Bengaluru, you can now approach your jurisdictional PCIT/CIT for condonation.

?tmstv=1774296112&v=7401Practical Action Points for You

- Identify your Jurisdictional PCIT/CIT (the one having jurisdiction over your trust’s PAN).

- File an application for condonation (letter + reasons + supporting documents) before the jurisdictional PCIT/CIT.

- Once condoned, the application will be treated as filed within time and CPC Bengaluru will process the registration.

- Director (CPC) Bengaluru has already been requested by CBDT to enable necessary system facility.

Conclusion

Earlier, many trusts were facing rejection or endless back and forth between local officers and CPC Bengaluru. This circular ends that confusion and gives a clear, single-window authority (jurisdictional PCIT/CIT) to grant relief.

If your trust missed the deadline for Form 10A and you have a genuine reason (change of auditor, technical glitch, first-time filing, etc.), act now — approach your jurisdictional PCIT/CIT immediately.

Pro Tip: Mention “CBDT Circular No. 01/2026 dated [issue date]” in your condonation application for faster processing.