New TDS Compliance: UIN (Unique Identification Number)

The Income-tax compliance landscape is shifting towards a digital environment. Notification No. 01/CPC(TDS)/2026 (dated 28 March 2026) introduces a rigorous new mechanism for handling nil TDS declarations under Section 393(6). Whether you are a deductor (payer) or a taxpayer submitting Form 121, this update is a critical compliance checkpoint. Effective 1 April 2026, “trust-based” declarations are officially being replaced by a digital, traceable ecosystem.

The Basics: What is Form 121?

Under the Income-tax Act, 2025, Section 393(6) allows for non-deduction of TDS if the recipient (payee) declares their total income is NIL.

- The New Standard: Form 121 is the modern successor to the old Form 15G/15H.

- The PAN Mandate: Under Section 397(1)(f), a valid PAN is not optional. If PAN is missing, the declaration is invalid, and TDS must be deducted at higher rates.

Relevant Statutory Provisions

Section 393(6) – Provides for Non-deduction of TDS after obtaining declaration

The deduction of tax shall not be made under provisions referred to in column C of the Table below, in the case of a person as specified in column B, if such person furnishes to the person responsible for paying any income or sum of the nature referred to in such provisions, a written declaration in duplicate in such form and manner as may be prescribed that the tax on such person’s estimated total income of the tax year in which such income or sum is to be included in computing his total income shall be nil.

Section 397(1)(f) – Provides for Non-deduction of TDS after obtaining declaration

f a person does not furnish his valid Permanent Account Number in—

(i) any declaration under section 393(6) or 394(2), then such declaration becomes invalid;

(ii) any application made under provisions of section 395(1) or (3), then no certificate under such provisions shall be granted;

Rule 211 – Provides for Non-deduction of TDS after obtaining declaration

1) A declaration under section 393(6) shall be furnished in Form No. 121.

(2) The declaration referred to in sub-rule (1) may be furnished in any of the following manner:—

a. electronically after duly verifying through an electronic process; or

b. in paper form.(3) The person responsible for paying any income or sum of any nature referred to in section 393(6), shall allot a unique identification number to each declaration received by him in Form No. 121, during every quarter of the financial year in accordance with the procedures, formats and standards specified by the Director General of Income-tax (Systems).

📄 Download Official Notification

Get the complete Notification No. 01/CPC(TDS)/2026 with full procedural details on Form 121 and UIN compliance.

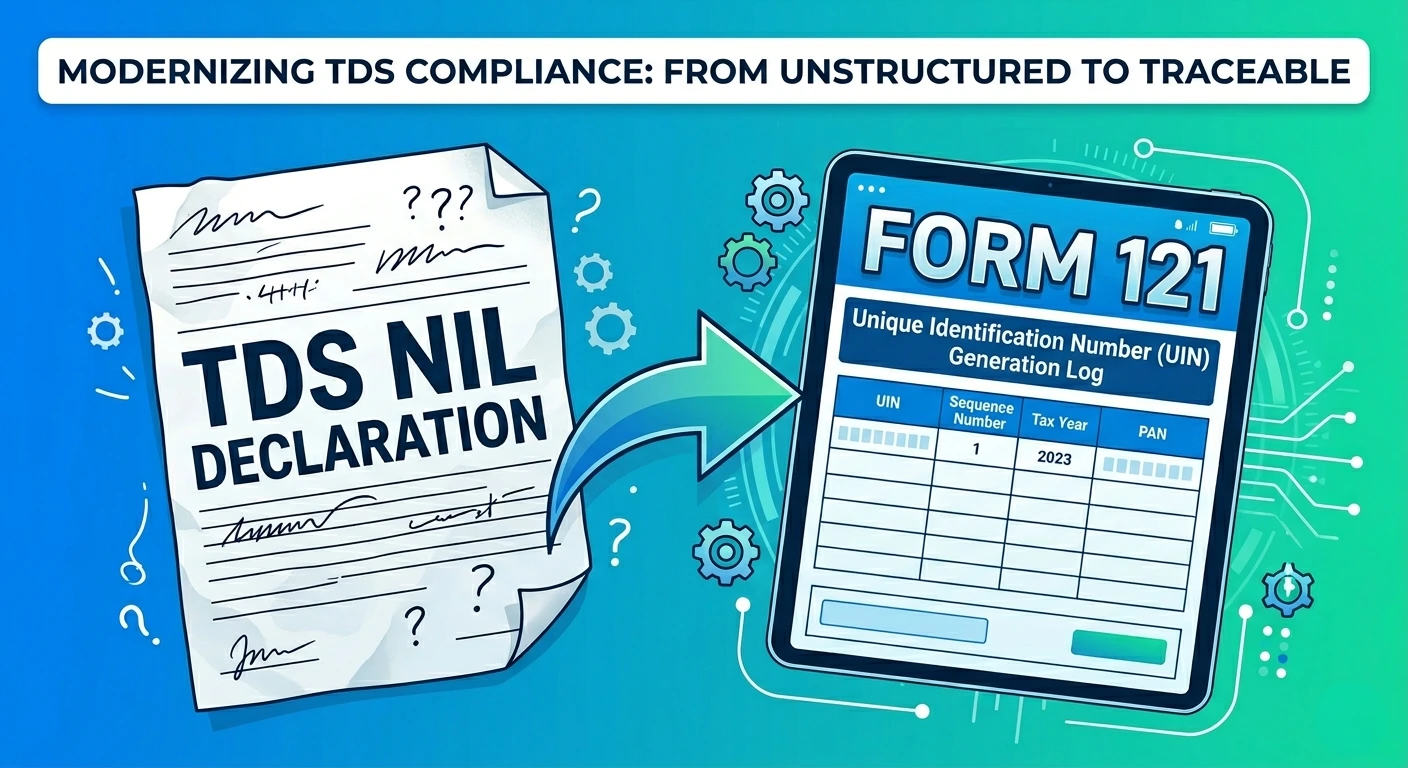

The New 26-Character UIN (Unique Identification Number)

The most significant change is the mandatory allotment of a UIN by the payer for every Form 121 received. This acts as a digital fingerprint for every declaration.

UIN Structure – Decoded

The sequence resets to “D000000001” at the start of every tax year for each TAN.

| Field | Length | Example | Description |

| Sequence Number | 10 | D000000001 | Starts with “D” + 9 digits |

| Tax Year | 6 | 202627 | For Tax Year 2026–27 |

| TAN of Payer | 10 | MUMN12345A | 10-character TAN of the deductor |

Full UIN Example: D000000001202627MUMN12345A

Compliance Checklist for Deductors (Payers)

The burden of compliance has increased significantly. Ensure your systems are ready for these four pillars:

- Immediate Allotment: Assign a UIN as soon as a valid Part A of Form 121 is received.

- Mandatory Digitization: Physical paper forms must be digitized and assigned the next running sequence number in your digital log.

- Quarterly Reporting: You must report all UINs in your quarterly statement (Rule 219), even if no tax was deducted during that period.

- 7-Year Retention: All declarations (paper or digital) must be preserved for verification for 7 years.

📑 Form 121 (Section 393(6)) – Ready-to-Use Declaration Formats

Use this format to obtain NIL TDS declarations from eligible persons (replacing earlier Form 15G / 15H usage).

⚠️ Important Update

Practical Impact: What Changes for You?

🧑💼 For Taxpayers (Payees)

- Accuracy is Key: Ensure your income estimation is precise; digital tracking makes audit triggers more likely.

- PAN Validity: Double-check that your PAN is linked and active to avoid immediate TDS deduction.

🏢 For Businesses / Accounts Teams

- Software Updates: Update your ERP or TDS software to automate the 26-character UIN generation.

- Centralized Logs: Maintain a single sequence for both paper and electronic forms to avoid numbering conflicts.

Frequently Asked Questions (FAQs)

📈 Why This Matters

This move signals a shift from “loose paper slips” to digitally traceable assets. Each declaration is now stamped, tracked, and auditable in real-time by the CPC-TDS system.

🔗 Related Resources

- Income Tax Act, 2025: Full Guide

- Notifications under the Income Tax Act, 2025

- Compliance Calendar – April 2026