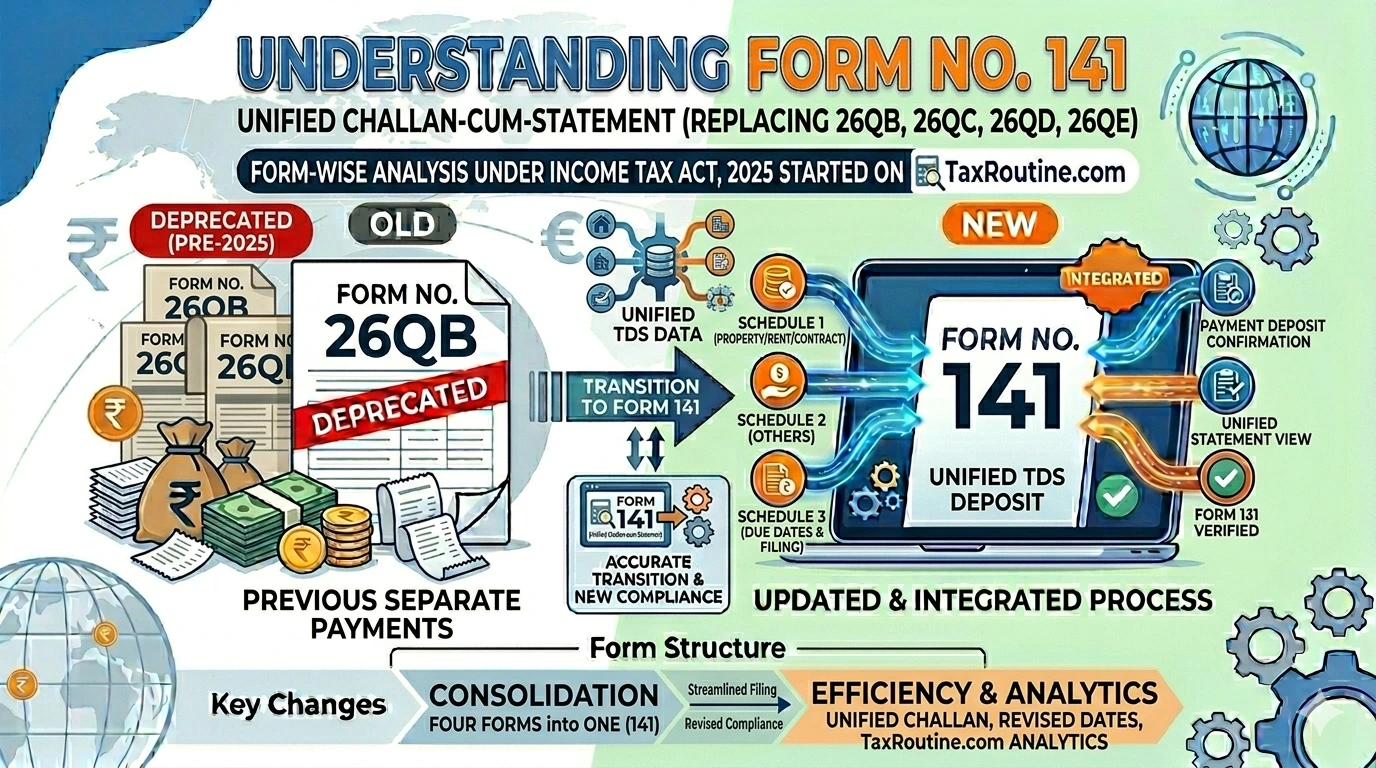

Quick summary: The four separate PAN-based challan-cum-statements — Forms 26QB (property), 26QC (rent), 26QD (professionals/contractors), and 26QE (virtual digital assets) — are now consolidated into a single unified form: Form No. 141. Each transaction type is handled through a dedicated schedule within the form. No TAN is required. Filing is done using the deductor’s PAN, and tax is paid simultaneously at the time of filing.

📋 Quick Reference

Old Form Names26QB, 26QC, 26QD, 26QE

New Form NameForm No. 141

Old RulesRules 30 & 31A, I.T. Rules 1962

New RulesRules 218 & 219, I.T. Rules 2026

Old Sections194-IA, 194-IB, 194M & 194S

New SectionsSection 393(1) [Table Sl. Nos. 2(i), 3(i), 6(ii), 8(vi)]

Form TypeChallan-cum-Statement (no separate challan)

TAN Required?No — PAN-based filing

Due DateWithin 30 days from end of month of deduction

Under the old framework, individuals and HUFs who deducted TDS on specific high-value transactions had to navigate four completely separate forms — 26QB for property, 26QC for rent, 26QD for payments to contractors/professionals, and 26QE for virtual digital assets. Each had its own structure, filing mechanism, and compliance logic.

Form No. 141 consolidates all four into a single, schedule-based challan-cum-statement. The deductor selects the relevant schedule, fills only that portion, and pays TDS simultaneously — making compliance significantly simpler for individuals and HUFs who are not required to hold a TAN.

Combined, the four old forms had approximately 17–18 lakh annual filings (26QB: 16–17 lakh, 26QC: 80–85 thousand, 26QD: 6 thousand, 26QE: 4–5 thousand). Form No. 141 unifies all of this under one roof.

2The Four Schedules — At a Glance

Form No. 141 has four schedules, each corresponding to a specific transaction type. Only the schedule relevant to the deductor’s transaction needs to be filled — not all four.

Schedule A

TDS on Rent

Erstwhile Form 26QC

Section 393(1) [Table Sl. No. 2(i)]

TDS on rent paid by an individual or HUF to a resident landlord on land, building, or both.

Threshold: > ₹50,000 per month

Filed by: Tenant (individual/HUF)

Schedule B

TDS on Property Purchase

Erstwhile Form 26QB

Section 393(1) [Table Sl. No. 3(i)]

TDS on payment for transfer of immovable property (other than agricultural land) to a resident seller.

Threshold: ₹50 lakh or more

Filed by: Buyer of property

Schedule C

TDS on Professionals & Contractors

Erstwhile Form 26QD

Section 393(1) [Table Sl. No. 6(ii)]

TDS by an individual or HUF not liable to audit on payments to residents for contract work, commission, brokerage, or professional fees.

Threshold: Aggregate > ₹50 lakh in Tax Year

Filed by: Individual/HUF payer (non-audit)

Schedule D

TDS on Virtual Digital Assets

Erstwhile Form 26QE

Section 393(1) [Table Sl. No. 8(vi)]

TDS on consideration paid for transfer of a Virtual Digital Asset (cryptocurrency, NFT, etc.) to a resident transferor.

Threshold: No monetary limit

Filed by: Buyer/payer of VDA consideration

Only one schedule may be filled per Form No. 141 filing. If you have two different types of transactions — say, a property purchase and a rent payment — you file two separate Form No. 141s, one for each schedule.

3Form No. 141 vs Form No. 140 — A Critical Distinction

Both forms deal with non-salary TDS, but they serve very different deductors and operate on entirely different mechanics.

Form No. 140 (Erstwhile 26Q)

Quarterly statement — covers multiple deductees and transactions in one return

TAN mandatory — filed by businesses, companies, firms, banks

Tax deposited separately via challan before filing the statement

Filed via RPU + FVU utility, uploaded to e-filing portal

Covers broad range of non-salary income types

Generates Form No. 131 as TDS certificate

Form No. 141 (Erstwhile 26QB/QC/QD/QE)

Per-transaction filing — one form per transaction type per month

PAN-based — no TAN needed; primarily for individuals and HUFs

Tax deposited simultaneously at the time of filing the form

Filed directly via e-Pay Tax on the e-filing portal

Covers only four specific transaction types via four schedules

Generates Form No. 132 as TDS certificate

4Due Date and Filing Frequency

Unlike Form No. 138 or Form No. 140 which follow fixed quarterly due dates, Form No. 141 has a transaction-driven due date:

Due date: Within 30 days from the end of the month in which TDS was deducted. For example, if TDS on a property purchase was deducted on 15th May, Form No. 141 (Schedule B) must be filed by 30th June.

Transactions with different months of deduction cannot be clubbed in a single Form No. 141. Each month’s deduction for the same transaction type requires a separate filing.

5Multiple Buyers/Sellers — Status Rules

A significant practical improvement in Form No. 141 is the handling of transactions involving multiple parties. The key rule is based on the status (company or non-company) of the deductees:

⚖️ Same-Status Rule — How to File When Multiple Parties Are Involved

If all deductees (sellers/landlords/service providers) have the same status (all companies or all non-companies), the deductor files one Form No. 141 covering all of them collectively.

If deductees have different statuses (some companies, some non-companies), the deductor must file separate forms — one for company deductees and one for non-company deductees.

This applies to all four schedules — rent (A), property (B), professionals (C), and VDA (D).

This is a significant improvement over the old framework — under Form 26QD (the old Schedule C equivalent), a deductor making payments to multiple deductees in the same month had to file a separate form for each deductee. Under Form No. 141, same-status deductees can now be reported in one consolidated form.

6How to File Form No. 141

1

Log in to the Income Tax e-Filing Portal using PANNo TAN login required. Use your own PAN credentials at incometax.gov.in.

2

Go to e-Pay Tax and select Form No. 141Navigate to the e-Pay Tax section and select the relevant schedule — A (rent), B (property), C (professional/contractor), or D (VDA).

3

Fill deductor and deductee detailsEnter PAN, address, contact, and email of both parties. For property (Schedule B) and rent (Schedule A), enter the property address and share percentages of all buyers/sellers or tenants/landlords.

4

Enter transaction detailsFill in the relevant transaction data — rent amount and period (A), stamp duty value and sale consideration (B), nature of service and aggregate payment (C), or VDA type, transfer date, and consideration (D).

5

Pay TDS and submitMake online TDS payment simultaneously with form submission. On successful payment, a Challan Identification Number (CIN) is automatically generated against the acknowledgement number.

6

Download the challan-cum-statementDownload and retain the submitted form as proof. The ARN (Acknowledgement Receipt Number) is also generated on submission. TDS certificate in Form No. 132 can be downloaded from TRACES after processing.

7What Happens After Filing?

Form No. 132 is generated (TDS Certificate)Upon successful processing, the deductor can download Form No. 132 from TRACES — the TDS certificate specific to Form No. 141 transactions. It must be issued to the deductee within 15 days from the due date of filing Form No. 141.

TDS reflects in deductee’s Form No. 168The TDS amount appears in the deductee’s (seller’s/landlord’s/service provider’s) Form No. 168 (AIS), enabling them to claim the credit when filing their ITR.

Defaults or correctionsIf the statement is processed with defaults (short payment, late interest, late fee), the deductor must pay the default amount and file a correction statement within two years from the end of the Tax Year.

8Key Changes from the Old Forms to Form No. 141

Old Forms: 26QB / 26QC / 26QD / 26QE

Four separate forms — four separate filing processes

26QD required a separate form per deductee per month for professional payments

No consolidated reporting for multiple buyers/sellers in one property transaction

No consolidated reporting for VDA transactions with multiple parties

Terminology: “Assessment Year / Financial Year”

Currency symbol: Rs.

Manual data entry throughout

Form No. 141 (New)

✅ Single unified form with four schedules — one filing process

✅ Schedule C: one form covers multiple same-status deductees per month per nature of payment

✅ All buyers and sellers in a property transaction can be reported in one form (if same status)

✅ VDA transactions with multiple same-status parties in one form

Professional / contract / commission / brokerage (by non-audit individual/HUF)

Aggregate > ₹50 lakh in the Tax Year

D

Transfer of Virtual Digital Asset (VDA)

No monetary threshold — every transfer

10Penalties for Non-Compliance

🚨

Late Filing Fee — Section 427

Late filing of Form No. 141 attracts a fee under Section 427 of the Income-tax Act, 2025. The fee applies from the date the deduction was required to be made to the date of filing.

💸

Interest on Late Deduction or Payment — Section 398(3)(a)

Interest under Section 398(3)(a) is levied for late deduction or late payment of TDS. This is separate from the late filing fee and continues to accrue until the TDS is deposited.

If a deductee’s PAN is invalid or incorrect in Form No. 141, the TDS credit will not reflect in their Form No. 168, and the deductor will be liable to deduct TDS at the higher rate under Section 397(2). Always verify PAN before filing.

11Frequently Asked Questions

It depends on the status of the sellers. If both sellers are individuals (non-companies), you file one Form No. 141 (Schedule B) covering both sellers with their respective share percentages. If one seller is a company and the other is an individual, you must file two separate forms — one for the company seller and one for the individual seller.

No. Each Form No. 141 filing covers only one schedule (one transaction type). If you have a property purchase and a rent payment in the same month, you need to file two separate Form No. 141s — one using Schedule B and one using Schedule A.

The deductee receives Form No. 132 — not Form No. 131. Form No. 132 is specifically generated from Form No. 141 transactions and covers TDS on property, rent, professional payments, and VDA transfers. The deductor must download it from TRACES and issue it to the deductee within 15 days of the Form No. 141 due date.

No. Schedule C applies only when the aggregate payment exceeds ₹50 lakh in a Tax Year to resident contractors, professionals, or commission/brokerage agents — and only if you are an individual or HUF not required to deduct TDS under any other provision (i.e., you are not liable to tax audit). A payment of ₹45 lakh does not trigger Schedule C.

Yes. A correction statement may be filed to rectify errors in any schedule. The correction window is two years from the end of the Tax Year in which the original statement was required to be filed.

No. Unlike the other three schedules, Schedule D has no monetary threshold. TDS must be deducted on every transfer of a Virtual Digital Asset where consideration is paid to a resident transferor, regardless of the amount.

Download Form No. 141

Access the official CBDT-notified form in PDF format.

CA Final Student & Semi-Qualified Chartered Accountant

Ruban Jayakumar is a CA Final student and semi-qualified Chartered Accountant specializing in taxation, accounting, and finance. With over five years of experience in tax litigation before appellate forums, he works closely with businesses and individuals to simplify complex tax and compliance matters. Through TaxRoutine, he shares practical insights aimed at making taxation accessible and understandable for the general public.