Blocked Credits Under Section 17(5)

of the CGST Act: The Complete Guide

Motor vehicles, food, construction, personal expenses — the categories where ITC is denied by law, and the exceptions that most businesses overlook.

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- Part 2 — Section 16: Conditions for Claiming ITC

- ▶ Part 3 — Blocked Credits under Section 17(5) (You are here)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- Part 6 — ITC Reversal under Rule 37: Practical Difficulties

- Part 7 — Input Service Distributors (ISD) under GST

📌 At a Glance

- Section 17(5) of the CGST Act lists categories where ITC is statutorily blocked — regardless of business use or valid invoice.

- Major categories: motor vehicles, food & beverages, outdoor catering, beauty treatment, health services, club memberships, works contract for immovable property, and goods/services for personal consumption.

- Each blocked category carries specific exceptions — the devil is in the detail.

- Wrongly claimed blocked ITC attracts recovery + 18% interest under Section 50 + penalty under Sections 73/74.

- The CBIC has issued multiple clarificatory circulars on Section 17(5) — latest positions are reflected in this post.

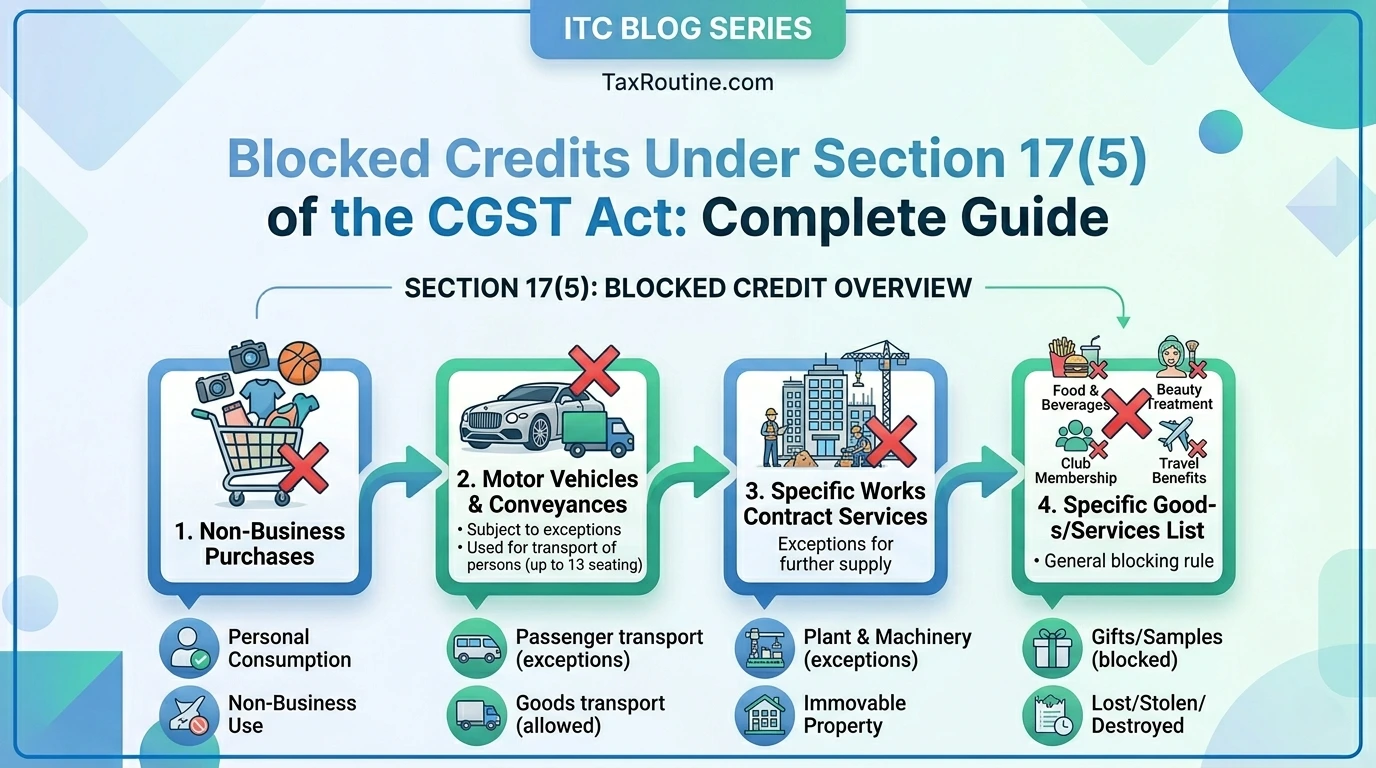

1. What Are Blocked Credits?

Under the GST framework, ITC is the default right of every registered person for goods and services used in business. Section 17(5) is the exception — it carves out a list of specific categories where the legislature has decided, as a matter of policy, that ITC will not be available even if the goods or services are used in the course of business and a valid tax invoice exists.

These are commonly referred to as “blocked credits” or “ineligible ITC”. They must be reported separately in Table 4(D) of GSTR-3B — businesses are expected to identify and self-report ineligible ITC rather than wait for a notice. Returns are filed through the GST portal at gst.gov.in.

The policy rationale is to prevent ITC from being claimed on expenditure that is in the nature of final consumption rather than business input — for example, a director’s food bill or a company car used for personal commuting. Allowing ITC on such expenses would effectively make the government subsidise private consumption through a business GST credit. Read the full text of Section 17 on CBIC.gov.in →

2. The Blocked Credit Categories — Section 17(5) in Detail

Below is each blocked category under Section 17(5) of the CGST Act with the exact scope of the block and the statutory exceptions.

Motor Vehicles & Other Conveyances

ITC is blocked on motor vehicles for transportation of persons having an approved seating capacity of not more than 13 persons (including the driver) — and on vessels and aircraft — along with services of general insurance, servicing, repair, and maintenance of such vehicles.

- Cars, SUVs, vans (≤13 seats) purchased for office use

- Motor insurance on company cars used by employees

- Service & maintenance of company cars

- Helicopters / aircraft for corporate travel

- Vehicles used for transportation of goods (trucks, tempo, lorry)

- Vehicles used for transportation of passengers as core business (taxi, bus operator, cab aggregator)

- Vehicles used for imparting driving training (driving schools)

- Further supply of such vehicles (automobile dealers)

- Vehicles with >13 seat capacity (buses, mini-buses)

Food, Beverages, Outdoor Catering & Personal Care

ITC is blocked on the following services and goods when received by a business for its own use or for employees:

- Food and beverages (office meals, team lunches)

- Outdoor catering (office parties, client events)

- Beauty treatment, health services

- Cosmetic and plastic surgery

- Membership of a club, health, and fitness centre

- Travel benefits to employees (vacation packages)

- Hotel making outward supply of food (restaurant business)

- Caterer supplying outdoor catering services (core business)

- Cosmetic surgery hospital making outward supply of surgery

- Gym / spa club making outward supply of fitness services

- Where obligatory under any law for the time being in force

Life Insurance, Health Insurance & Employee Transport

ITC is blocked on life insurance and health insurance procured for employees, and on cab / transportation services provided to employees for commuting, unless the employer is legally obligated to provide these benefits.

- Group life insurance for employees (voluntary benefit)

- Group health / mediclaim for employees (if not legally mandatory)

- Cab services for employee pick-up and drop (voluntary)

- Travel insurance for employee trips

- Insurance mandatory under Employees’ Compensation Act, 1923

- ESIC-covered medical services (statutory obligation)

- Transport services mandated by any applicable law

- Insurance companies making outward supply of insurance (core business)

Works Contract Services for Immovable Property

ITC is blocked on works contract services received for construction of an immovable property (including civil structure) — except where it is an input service for further supply of works contract service.

- Civil construction of factory or office building (own use)

- Works contract for renovation of existing premises (own use)

- Electrical works embedded in the building structure

- Waterproofing, interior fit-outs forming part of immovable property

- Works contract services received by a contractor for further supply of works contract (sub-contracting)

- Works contract for plant and machinery (not part of immovable property structure)

- Movable temporary structures / prefabricated units

Goods or Services for Construction of Immovable Property (Own Account)

ITC is blocked on goods or services — including goods forming part of the immovable property — used for construction on one’s own account, even where such property is subsequently used for making taxable supplies. The classic example is a manufacturer who constructs its own factory.

- Steel, cement, sand, bricks used in factory construction

- Architect and structural design fees for own building

- Labour charges for construction of office premises

- Lift installation embedded in building structure

- Real estate developer constructing for sale (prior to OC/first occupation)

- Plant and machinery installed in factory (not part of building)

- Temporary sheds and structures (movable, not immovable)

- Furniture and fittings that are not embedded in the structure

Tax Paid Under Composition Levy

A composition taxpayer who pays tax under Section 10 (the composition levy) cannot claim any ITC on their purchases. This is a blanket restriction — composition dealers collect no output tax from customers and hence have no ITC mechanism.

Goods or Services Received by a Non-Resident Taxable Person

A non-resident taxable person can claim ITC only on goods imported by them at the time of registration. ITC on any other inward supply of goods or services received during their period of registration in India is blocked.

Goods or Services Used for Personal Consumption

ITC is blocked on any goods or services used for personal consumption — i.e., not for business use. If a business buys something partly for business and partly for personal use, only the business-use portion qualifies for ITC.

- Groceries purchased through a business account for a director’s household

- Holiday trip for proprietor and family booked through the firm

- Home furnishings purchased on firm’s GSTIN for personal use

- Same goods if genuinely purchased and used for business operations

- Hospitality expenses for business clients (subject to other 17(5) checks)

Goods Lost, Stolen, Destroyed, Written Off, or Gifted

ITC is blocked — or must be reversed — on goods that are lost, stolen, destroyed, written off in the books, or disposed of by way of gift or free samples. If ITC was already claimed when the goods were purchased, it must be reversed in the month the goods are lost, destroyed, written off, or gifted.

3. The “Plant and Machinery” Carve-Out

One of the most important — and frequently misapplied — aspects of Section 17(5) is the exclusion of plant and machinery from the construction-related blocks under clauses (c) and (d). The law provides that ITC is not blocked on plant and machinery even when it is used in relation to immovable property. For a full treatment of capital goods ITC including plant and machinery, see Part 5 of this series.

The Explanation to Section 17 of the CGST Act defines “plant and machinery” as apparatus, equipment, and machinery fixed to earth by foundation or structural support — but excludes: land, building, and civil structures; telecommunication towers; and pipelines laid outside the factory premises.

A textile manufacturer sets up a new factory

Factory building construction (RCC, walls, roof): GST paid → ITC Blocked under Section 17(5)(d).

Electrical wiring embedded in walls: GST paid → ITC Blocked (forms part of immovable property).

Looms and weaving machines installed in factory: GST paid → ITC Allowed — plant and machinery, even though fixed to earth.

Air-conditioning plant (industrial HVAC): GST paid → ITC Allowed — classified as plant and machinery.

Lift installed in the building: GST paid → ITC Blocked — lift is part of the building structure (litigated area — some AAR rulings differ).

4. Real Estate Developer: The Critical Exception

The construction block under Section 17(5)(d) contains a vital proviso: ITC is available if the immovable property is constructed for making outward taxable supplies — i.e., for sale. This is the lifeline for real estate developers.

| Scenario | ITC on Construction? | Reason |

|---|---|---|

| Developer builds residential apartments for sale (before OC) | Allowed | Construction for outward taxable supply — exception applies |

| Developer sells flats after Occupancy Certificate (exempt supply) | Blocked | Post-OC sale is exempt — no taxable outward supply |

| Manufacturer builds own factory for production | Blocked | Construction not for further supply — own use; block applies |

| Commercial complex built for renting out (taxable supply) | Disputed | Renting is taxable, but several AAR rulings have denied ITC; litigation pending |

| Sub-contractor receiving works contract from main contractor | Allowed | Input service for further supply of works contract — express exception |

5. Key CBIC Clarifications on Section 17(5)

Circular No. 172/04/2022 — ITC on CSR Expenditure

The CBIC clarified through Circular No. 172/04/2022-GST that ITC is not available on goods or services procured for Corporate Social Responsibility (CSR) activities under Section 135 of the Companies Act, 2013 — as CSR expenditure does not qualify as being used “in the course or furtherance of business” for GST purposes.

Circular No. 206/18/2023 — ITC on Employee Perquisites

Circular No. 206/18/2023-GST reiterated that ITC on employee perquisites — cab services, meals, insurance — is blocked under Section 17(5) unless the provision of such services is obligatory under any law. Voluntary employer benefits do not unlock ITC.

ITC on expenses incurred in connection with issuing Employee Stock Options (ESOPs) — legal fees, accounting fees, merchant banker fees — is a grey area. The CBIC has not issued a specific clarification. Some advance rulings have denied ITC on the ground that ESOPs do not constitute a “supply” in the course of business. Approach with caution and seek professional advice.

6. Reporting Blocked Credits in GSTR-3B

Businesses are required to self-identify and report ineligible ITC in their GSTR-3B, filed through the GST portal. The relevant table is Table 4(D) — Ineligible ITC:

| Table in GSTR-3B | What to Report |

|---|---|

| Table 4(A) | Total ITC available (auto-populated from GSTR-2B) |

| Table 4(B) | ITC reversed (Rule 42, Rule 43, Rule 37, etc.) |

| Table 4(D)(1) | ITC on inward supplies on which Section 17(5) applies — blocked credits |

| Table 4(D)(2) | Other ineligible ITC not covered by Section 17(5) (e.g., used for exempt supplies) |

Failure to report blocked ITC in Table 4(D) — effectively claiming it as eligible ITC — is treated as a contravention of the CGST Act. It attracts recovery under Section 73 or 74, interest at 24% per annum under Section 50(3) from the date of incorrect claim, and a penalty of up to 100% of the tax in cases involving fraud or wilful misstatement.

7. Quick Reference: Blocked Credits at a Glance

| Category | Section | ITC Status | Key Exception |

|---|---|---|---|

| Motor vehicles (≤13 seats) + insurance + repair | 17(5)(a) | Blocked | Passenger transport business, goods transport, dealer |

| Food, beverages, outdoor catering | 17(5)(b)(i) | Blocked | Core outward supply of same service |

| Beauty treatment, health & fitness services | 17(5)(b)(ii) | Blocked | Core outward supply of same service |

| Life & health insurance for employees | 17(5)(b)(iii) | Blocked | Legally obligatory under any law; insurer’s own business |

| Travel benefits / employee cab services | 17(5)(b)(iv) | Blocked | Legally obligatory under any law |

| Works contract for immovable property construction | 17(5)(c) | Blocked | Sub-contracting; plant & machinery |

| Goods/services for immovable property (own account) | 17(5)(d) | Blocked | Construction for outward taxable supply (developer); plant & machinery |

| Composition taxpayer — all purchases | 17(5)(e) | Blocked | None — blanket block |

| Non-resident — inward supplies other than imports | 17(5)(f) | Blocked | Imports of goods at time of registration |

| Goods/services for personal consumption | 17(5)(g) | Blocked | None — business-use portion claimable separately |

| Goods lost, stolen, destroyed, written off, gifted | 17(5)(h) | Blocked | None — reversal mandatory |

| Club membership, health & fitness centre | 17(5)(b) | Blocked | Club itself making outward supply of membership services |

Frequently Asked Questions

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- Part 2 — Section 16: Conditions for Claiming ITC

- ▶ Part 3 — Blocked Credits under Section 17(5) (You are here)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- Part 6 — ITC Reversal under Rule 37: Practical Difficulties

- Part 7 — Input Service Distributors (ISD) under GST

Excellent breakdown of Section 17(5)! I have a specific scenario regarding employee wellness programs that I’m trying to clear up. Our firm is considering providing certain health-related supplements or specialized wellness products as part of a mandatory health initiative. Given the strict restrictions on “personal consumption”, would ITC be available if these are categorized as a safety requirement, or would they still fall under the blocked category? I was reading about some similar health-compliance products on https://pinupbdguide.com and wondered if the GST treatment changes when the items are technically part of a documented workplace wellness policy. Would love to hear your thoughts on this nuance.