In today’s fast-paced business environment, corporate agility is a competitive advantage. For group companies—specifically holding companies and their wholly-owned subsidiaries—the traditional merger process can often feel like a bureaucratic marathon.

However, Section 233 of the Companies Act, 2013 provides a “Fast Track” alternative. By bypassing the National Company Law Tribunal (NCLT) and obtaining approval directly from the Regional Director (RD), eligible companies can achieve synergy with significantly lower administrative overhead and accelerated timelines.

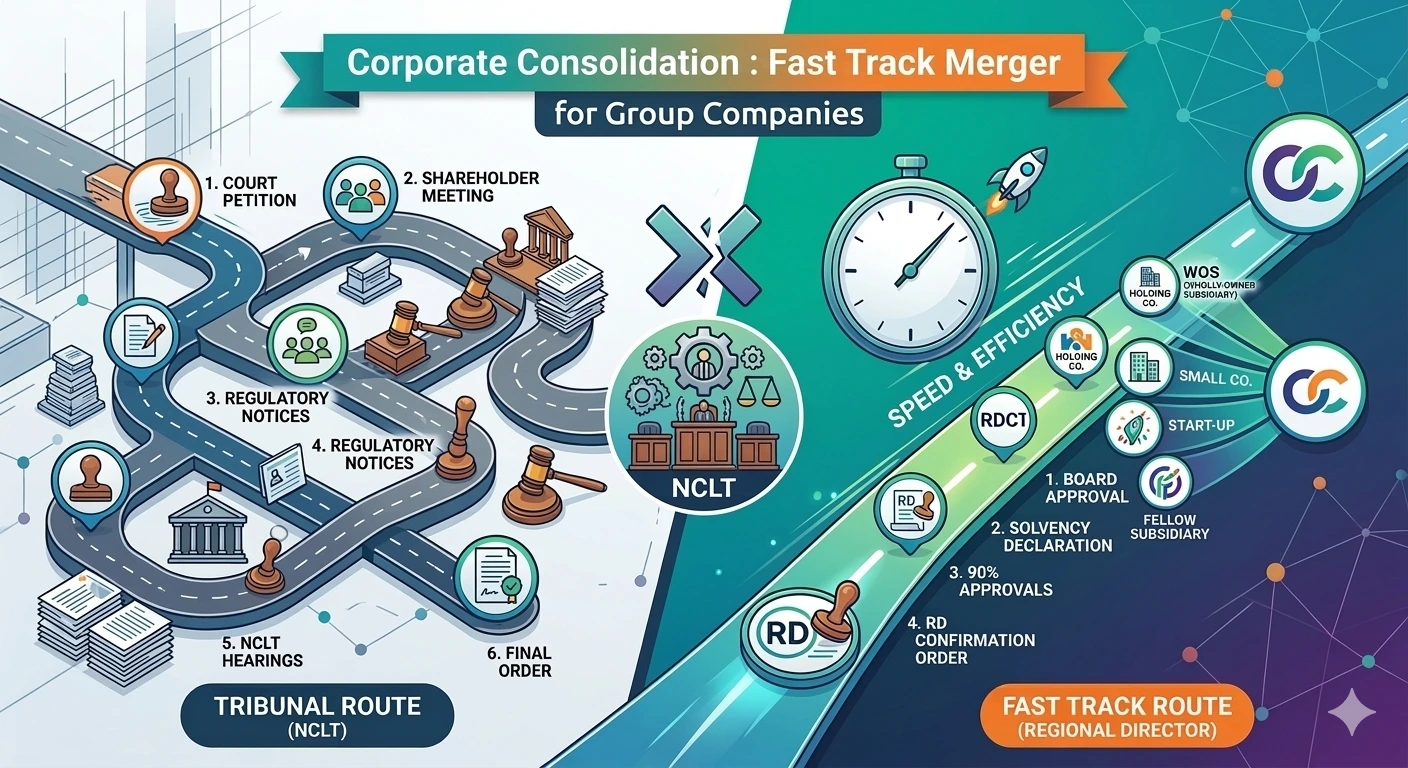

Fast-Track Merger under Section 233 – Quick Overview

A Fast-Track Merger under Section 233 of the Companies Act, 2013 allows certain classes of companies to merge without approaching the National Company Law Tribunal (NCLT). Instead, the scheme is approved by the Regional Director (RD) of the Ministry of Corporate Affairs.

Key features include:

• Applicable to small companies, holding companies and wholly-owned subsidiaries, startups, and certain unlisted companies.

• The merger is approved through member and creditor consent (90% threshold).

• The scheme is reviewed by the ROC and Official Liquidator before confirmation by the Regional Director.

• Once confirmed, the transferor company stands dissolved without winding-up.

Applicability of Fast Track merger

Fast Track Mergers (FTM) under Section 233(1) of the Companies Act, 2013, are tailored for select company classes to expedite restructuring while maintaining oversight. This provision, supported by Companies (Compromises, Arrangements and Amalgamations) Rules, enables schemes between:

- Two or more small companies or

- A holding company and its wholly-owned subsidiary or

- Two or more startup companies

(Note: Startup company means a private company incorporated under the Companies Act 2013 or the 1956 Act and as such recognized by the Department for Promotion of Industry and Internal Trade). - One or more startups with one or more small companies.

- One or more unlisted companies with another unlisted company (excluding Section 8 companies), where each has loans, debentures, or deposits not exceeding ₹200 crore and no repayment defaults.

- A holding company (listed or unlisted) and its subsidiary (listed or unlisted), provided the transferor company is unlisted.

- One or more subsidiaries of a holding company with other subsidiaries of the same holding, where transferors are unlisted.

- Merger of the transferor foreign company incorporated outside India being a holding company with the transferee Indian company being its wholly owned subsidiary company incorporated in India

- Eligible entities may opt for the standard Sections 230-232 NCLT route if preferred. Provisions extend, with modifications, to divisions or transfers. This framework, updated via 2025 MCA amendments, balances efficiency with eligibility safeguards.

Strategic Note

Engaging registered valuers and statutory auditors early is critical. Any discrepancies in share exchange ratios or eligibility certificates can inadvertently trigger the more complex Section 230-232 NCLT route.

For unlisted mergers, you must now include a mandatory Auditor’s Certificate (Form CAA-10A). This certifies that the debt thresholds and “no-default” status are satisfied within 30 days of the notice.

The Procedural Roadmap: A Step-by-Step Guide

The following sequence outlines the statutory journey of a Fast-Track Merger, optimized for executive oversight.

Phase 1: Initiation and Board Authorization

The process begins with a formal Board Meeting (BM). The Board must approve the merger scheme and authorize the filing of:

- Form CAA-9: The official notice of the scheme to invite objections or suggestions from the ROC and Official Liquidator (OL) or persons affected by the scheme within 30 Days [For Companies regulated by Sectoral Regulators like RBI/SEBI, the notice shall also be sent to the concerned regulator].

- Form CAA-10: A Declaration of Solvency filed by the companies along with the fee before convening the meeting of members and creditors for approval of the scheme. [an attachment to GNL-1]

- Form CAA-10A: The new mandatory Auditor’s Certificate (for unlisted/debt-cap cases).

- Form CAA-11: To be filed by the transferee company within 15 days after the conclusion of the meeting along with the report of the result with the Central Government, Registrar and the Official Liquidator. [as attachment to Form RD-1].

Phase 2: Stakeholder Consents & Regulatory Feedback

The Scheme must be approved by the Members and Creditors as follows:

- 90% Threshold: Secure approval from members holding 90% of total shares and creditors / class of creditors representing 90% in value. This can be done via a meeting or through written consent.

- Regulatory Objections: If the Registrar or Official Liquidator has any objections or suggestions, he may communicate the same in writing to the Central Government within a period of thirty days. If no objection is made, it shall be presumed that there is no objection to the scheme.

Phase 3: Public Compliance and Filings

Transparency is maintained through mandatory public disclosures:

- Website Publication: Notice and other documents be placed on the website of the company, if any, and in case of a listed company, these documents shall be sent to the Securities and Exchange Board and stock exchange where the securities of the companies are listed for placing on their website.

- Newspaper Publication: Notices must be published in both an English and a principal vernacular language newspaper.

- Form MGT-14: This must be filed within 30 days of passing the EGM resolution to certify shareholder approval.

Phase 4: Regional Director (RD) Oversight

In the Fast-Track route, the Regional Director (RD) takes on a central role, often replacing the need for extensive Central Government involvement.

- Form CAA-11: The petition (including the scheme and meeting reports) is filed with the RD within 15 days of the conclusion of the meetings (earlier, 7 days – Extended by the 2025 amendment).

- Form RD-1: Form CAA-11 is submitted as an attachment to this overarching application.

- Form GNL-1: A copy of the approve scheme is filed with the ROC in Form GNL-1 and with the Official Liquidator.

Phase 5: Final Approval and Implementation

Once the Regional Director and Registrar reports are reviewed and the hearing is concluded:

- Confirmatory Order (Form CAA-12) / Refer to NCL (Form CAA-13):

- If the Regional Director is satisfied, they issue a confirmation order within fifteen days after the expiry of the 30-day period. If objections are raised but are deemed not sustainable, the Central Government can still issue the confirmation order in Form No. CAA 12.

- Objections Raised: If they believe the scheme is against public or creditors’ interest, they may refer it to the NCLT n Form No. CAA.13 within 60 days of receiving the scheme, requesting the Tribunal to consider the scheme under Section 232.

- If a confirmation order is not received or file an application with the NCLT within sixty days of receiving the scheme, it shall be deemed that it has no objection to the scheme, and a confirmation order will be issued accordingly.

- The final confirmation order must be filed with the ROC in Form INC-28 on the MCA portal within 30 days of receipt of the order. Upon registration of the confirmation order, the transferor company stands dissolved without undergoing winding-up proceedings.

Key Compliance Timelines (2026 Example)

| Milestone | Expected Timeline | Executive Note |

|---|---|---|

| CAA-9 – Notice of Meeting | Jan 23, 2026 | U/s 230(3) to all classes |

| Form MGT-14 Filing | By Feb 15, 2026 | Within 30 days of EGM |

| Creditor List Finalization | Feb 27, 2026 | Essential for RD approval |

| INC-23 Filing (RD) | By Apr 12, 2026 | 1-month post-creditor notice |

| INC-28 Filing | Within 30 Days | Post-receipt of Final Order |

Effects of Registration of Merger

Upon registration of a Fast Track Merger scheme under Section 233(9) of the Companies Act, 2013, several key legal and operational effects take immediate effect, ensuring seamless corporate integration.

The key effects of registration are as follows:

- All the assets and liabilities of the transferor company becomes the assets and liabilities of the transferee company.

- If any charges are applicable on the properties of the transferor company, the same shall be enforceable as same on the properties of the transferee company.

- Any legal proceedings on or against the transferor company shall be continued against the transferee company.

- If the scheme covers payment to dissenting shareholders or creditors, any unpaid amounts become the liability of the transferee company.

These provisions facilitate a clean transfer without further shareholder or creditor action, underscoring the efficiency of the FTM route for eligible entities.

Conclusion

The Fast-Track Merger is a sophisticated tool for corporate agility. While it offers a streamlined path, the process requires meticulous documentation and rigid adherence to statutory timelines to avoid regulatory delays. For group companies, mastering this procedure is the key to seamless integration and long-term value creation.

FAQs

📘 Want to learn more?

All the filings with the OL shall be done in the Physical form ?