What is Input Tax Credit (ITC) Under GST?

A Plain-English Guide

The mechanism that prevents tax-on-tax — explained with examples, set-off rules, and everything a business owner or CA needs to know.

📌 At a Glance

- ITC lets registered businesses reduce output GST liability by the GST already paid on inputs.

- Governed primarily by Sections 16, 17, and 18 of the CGST Act, 2017.

- Available on goods, services, and capital goods — subject to conditions and restrictions.

- Not available to Composition taxpayers or for wholly exempt supplies.

- Set-off order: IGST first → CGST → SGST/UTGST.

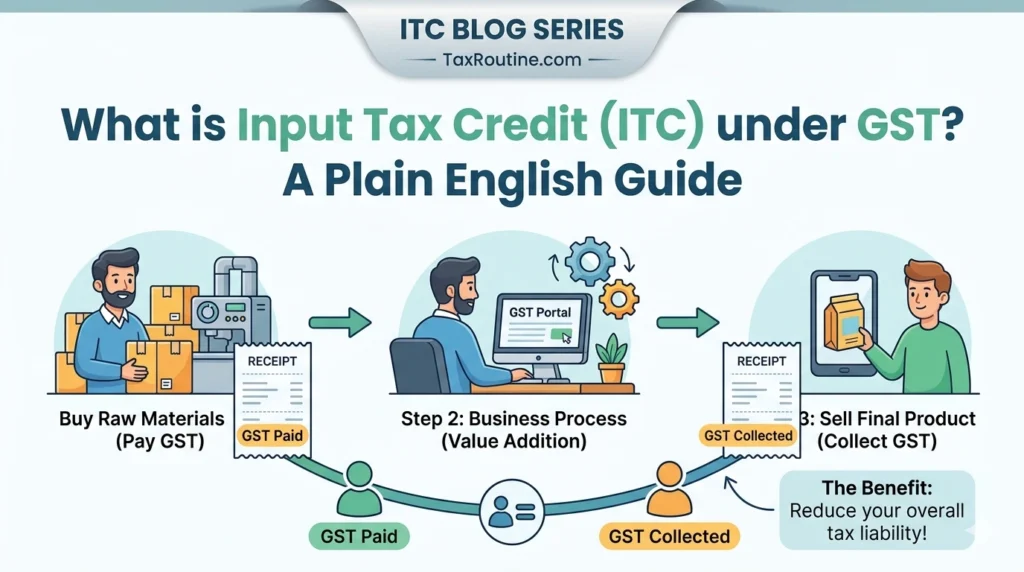

1. The Core Idea: What is ITC?

Every time a business buys something — raw materials, office supplies, machinery, professional services — it pays GST on that purchase. Without any relief mechanism, the business would pay GST again when it sells its own product or service. That would mean GST on top of GST, compounding the tax burden up the supply chain.

Input Tax Credit (ITC) is the mechanism that prevents this. Under the GST framework, a registered business can claim credit for the GST it has paid on its inward supplies (purchases) and use that credit to set off the GST it must collect on its outward supplies (sales). Only the net GST — after deducting the credit — is paid to the government.

Section 2(63) of the CGST Act, 2017 defines “input tax” as the central tax, state tax, integrated tax, or Union Territory tax charged on any supply of goods or services or both made to a registered person — including IGST on imports of goods.

A manufacturer buys steel and sells machinery

Step 1 — Purchase: Manufacturer buys steel worth ₹10,00,000. Supplier charges 18% GST = ₹1,80,000 (paid as input tax).

Step 2 — Sale: Manufacturer sells machinery worth ₹15,00,000. GST at 18% = ₹2,70,000 (output tax liability).

Step 3 — Set-off: Output tax (₹2,70,000) − ITC claimed (₹1,80,000) = ₹90,000 net GST payable to government.

Without ITC: the manufacturer would pay ₹2,70,000. With ITC: only ₹90,000. The system taxes only the value added at each stage.

2. Types of Input Tax: CGST, SGST, IGST

GST in India operates on a dual-structure: Central GST (CGST) and State GST (SGST) apply on intra-state transactions; Integrated GST (IGST) applies on inter-state transactions and imports. ITC can be claimed under all three, but the set-off order is governed by law.

| Available ITC | Set off against IGST | Set off against CGST | Set off against SGST/UTGST |

|---|---|---|---|

| IGST Credit | 1st priority ✔ | 2nd priority ✔ | 3rd priority ✔ |

| CGST Credit | ✔ (after IGST exhausted) | ✔ (after IGST) | ✘ Cannot cross-utilise |

| SGST/UTGST Credit | ✔ (after IGST exhausted) | ✘ Cannot cross-utilise | ✔ (after IGST) |

CGST credit cannot be used to pay SGST liability, and vice versa. IGST credit is the most flexible — it can be used against all three heads in the priority order above. Cross-utilisation between CGST and SGST is prohibited.

3. Who Can Claim ITC?

ITC is available to every registered person under GST — but with important carve-outs:

| Taxpayer Type | Can Claim ITC? | Reason / Note |

|---|---|---|

| Regular GST registrant (taxable supplies) | Yes | Full ITC available subject to conditions in Section 16 |

| Composition scheme taxpayer | No | Composition dealers pay tax at flat rate and are explicitly excluded from ITC |

| Businesses making only exempt supplies | No | No output tax to set off against; ITC must be reversed |

| Businesses with mixed (taxable + exempt) supplies | Partial | ITC proportionate to taxable use; balance reversed under Rule 42/43 |

| Input Service Distributor (ISD) | Distribute | Can receive and distribute ITC to branches but not consume directly |

| Non-resident taxable person | Limited | ITC only on imports of goods; restricted period |

4. What Can ITC Be Claimed On?

ITC is available on three broad categories of inward supply:

Inputs (Raw materials / goods purchased for business use)

Any goods purchased and used (or intended to be used) in the course or furtherance of business. Examples: raw materials for a manufacturer, trading stock for a trader, consumables used in production.

Input Services (Services received for business use)

Any services received and used in the course or furtherance of business. Examples: legal fees, accounting services, freight, IT services, advertising. Note: certain services are blocked under Section 17(5).

Capital Goods (Plant, machinery, equipment)

Goods capitalized in the books of accounts — machinery, computers, tools. ITC is available in full in the year of receipt (unlike earlier VAT regime which required spreading over time). Subject to reversal rules on disposal or change in use.

5. What ITC Is Not Available On

Section 17(5) of the CGST Act, 2017 lists specific categories where ITC is blocked regardless of business use. These are commonly called “blocked credits”. Key examples include:

| Category | ITC Status | Exception (if any) |

|---|---|---|

| Motor vehicles (seating capacity ≤ 13 persons incl. driver) | Blocked | Allowed if used for transport of passengers as core business, training, or further supply of vehicles |

| Food & beverages, outdoor catering, beauty treatment | Blocked | Allowed if making outward supply of the same category |

| Club memberships, health & fitness services | Blocked | None |

| Works contract services for immovable property construction | Blocked | Allowed if used for further supply of works contract services |

| Goods or services for personal consumption | Blocked | None |

Part 2 covers the four mandatory conditions under Section 16 in detail — the invoice, the payment-to-supplier rule, the return-filing requirement, and the receipt of goods. Part 3 is a full deep-dive into Section 17(5) blocked credits with case-law references. Don’t miss Part 4 on ITC reversal and interest under Section 50.

6. How ITC Is Claimed: The Basic Process

Receive a valid tax invoice from a GST-registered supplier

The supplier must be registered and the invoice must contain the mandatory particulars under Rule 46 of the CGST Rules.

Verify the credit in GSTR-2B

GSTR-2B is a system-generated auto-populated statement of ITC available to a buyer based on the supplier’s filed returns. ITC is available only for invoices reflecting in GSTR-2B as per the current legal framework.

Reconcile with your purchase register

Match GSTR-2B data with your books. Mismatches arise when suppliers have not filed returns, filed with errors, or the invoice period differs from your books.

Claim in GSTR-3B

Report the eligible ITC in Table 4 of GSTR-3B for the relevant period. The credit reduces the net GST payable. If credit exceeds liability, the balance accumulates as an electronic credit ledger balance.

Reverse ineligible ITC

Any ITC claimed in excess, on blocked items, or against which payment has not been made to the supplier within 180 days, must be reversed — and interest under Section 50 may apply.

7. Key Terms at a Glance

| Term | Meaning |

|---|---|

| Input Tax | GST charged on any supply made to a registered person (defined u/s 2(63) CGST Act) |

| Input Tax Credit (ITC) | The credit of input tax available for set-off against output tax liability |

| Electronic Credit Ledger | The GST portal ledger where ITC is credited and maintained; used for set-off |

| GSTR-2B | Auto-populated monthly statement of available ITC based on supplier filings |

| Blocked Credit | ITC that is statutorily denied under Section 17(5) despite being used in business |

| Input Service Distributor (ISD) | A registered office that receives common invoices and distributes ITC to branches |

| Rule 42/43 | Rules governing proportionate reversal of ITC where supplies are both taxable and exempt |

| Output Tax | GST chargeable on a taxable supply made by a registered person (excluding reverse charge) |