ICAI Widens Mandatory Scope of AQMM v2.0 — What Every CA Firm Must Know

The Institute of Chartered Accountants of India has issued an important clarification expanding who must comply with the Audit Quality Maturity Model — and for many firms, the clock started on April 1, 2026.

Background: What Is AQMM?

The Audit Quality Maturity Model (AQMM) is a framework introduced by ICAI to assess and improve the quality infrastructure of CA firms. It evaluates a firm’s policies, processes, technology usage, and governance across various maturity levels — essentially functioning as a self-assessment and benchmarking tool for audit quality.

AQMM version 2.0 was introduced to align Indian audit firms with global quality standards and is embedded within ICAI’s Peer Review mechanism. Firms are required to achieve a certain AQMM maturity level before or during their Peer Review.

Until now, AQMM was mandatory only for firms directly auditing listed entities, certain banks, and insurance companies. The April 2026 announcement significantly broadens this scope.

What Has Changed — The April 10, 2026 Announcement

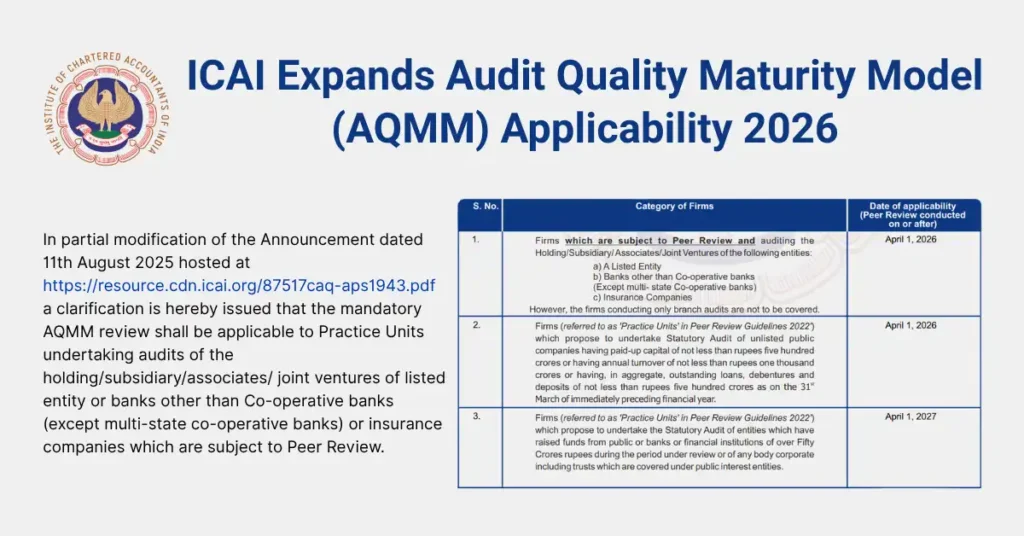

In partial modification of its earlier August 11, 2025 announcement, ICAI has clarified and expanded the mandatory applicability of AQMM. The key change: firms auditing the holding companies, subsidiaries, associates, or joint ventures of listed entities, banks, and insurance companies are now also covered — provided they are subject to Peer Review.

New Mandatory Categories & Effective Dates

AQMM v2.0 has been made mandatory in a phased manner for the following three categories of firms:

| S.No. | Category of Firms | Effective Date |

|---|---|---|

| 1 |

Firms subject to Peer Review and auditing the Holding / Subsidiary / Associates / Joint Ventures of: (a) A Listed Entity (b) Banks other than co-operative banks (except multi-state co-operative banks) (c) Insurance Companies Note: Firms conducting only branch audits are excluded. |

April 1, 2026 |

| 2 |

Firms proposing to undertake Statutory Audit of unlisted public companies with any one of the following: • Paid-up capital ≥ ₹500 crores, OR • Annual turnover ≥ ₹1,000 crores, OR • Outstanding loans, debentures & deposits ≥ ₹500 crores as on 31st March of the immediately preceding FY |

April 1, 2026 |

| 3 | Firms proposing to undertake Statutory Audit of entities that have raised funds from the public, banks or financial institutions exceeding ₹50 crores during the period under review, or any body corporate including trusts covered under public interest entities. | April 1, 2027 |

Key Highlights at a Glance

Who Is Excluded?

Important Exclusions to Note

- Branch Auditors: Firms conducting only branch audits of the above entities are explicitly excluded from mandatory AQMM compliance across all categories.

- Co-operative Banks: Banks organised as co-operative banks remain excluded — except multi-state co-operative banks, which are included.

Practical Implications for CA Firms

If your firm is subject to Peer Review and you have taken on any of the audit engagements described above, AQMM v2.0 compliance is no longer optional. Here is what this means practically:

- Complete your AQMM v2.0 self-assessment on the ICAI portal before your next Peer Review is scheduled.

- Firms auditing subsidiaries or associates of listed groups — even if the subsidiary itself is unlisted — are now covered under Category 1.

- Review your client list: if any client is a JV or associate of a listed entity, bank, or insurer, AQMM applies to your firm from April 1, 2026.

- For unlisted public companies, check the three financial thresholds (capital, turnover, debt) as on March 31 of the previous FY.

- Category 3 firms (>₹50 Cr fund-raise / public interest entities) have until April 1, 2027 — but early adoption is advisable.

Frequently Asked Questions

Conclusion

The widening of AQMM v2.0’s mandatory scope is a significant step by ICAI in raising the bar for audit quality across a much larger universe of firms. By extending coverage to firms auditing subsidiaries, associates, and JVs of listed entities and financial institutions, ICAI aims to ensure that audit quality frameworks percolate through the entire group audit ecosystem — not just at the top.

If your firm falls under Categories 1 or 2, the deadline has already passed — compliance should be in order now. For Category 3 firms, you have until April 2027, but early action is strongly recommended to avoid last-minute gaps during Peer Review.

Need Help with Audit Compliance or ICAI Requirements?

Our team at TaxRoutine stays on top of every ICAI and regulatory update so you don’t have to. Reach out for guidance on compliance frameworks, audit support, and more.

Talk to Our Experts →