Section 16 of the CGST Act:

Conditions for Claiming Input Tax Credit

Four conditions. All mandatory. Miss any one and the credit is lost — along with potential interest and penalties.

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- ▶ Part 2 — Section 16: Conditions for Claiming ITC (You are here)

- Part 3 — Blocked Credits under Section 17(5)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- Part 6 — ITC Reversal under Rule 37: Practical Difficulties

- Part 7 — Input Service Distributors (ISD) under GST

📌 At a Glance

- Section 16(2) prescribes four cumulative conditions — all must be satisfied to claim ITC.

- Holding a valid tax invoice is the first and most basic requirement.

- The 180-day payment rule (Rule 37) mandates reversal of ITC if the supplier is not paid within 180 days of the invoice date.

- ITC is contingent on the supplier actually paying tax to the government (tracked via GSTR-2B).

- Section 16(4) sets a hard time limit — ITC lapses if not claimed by the November GSTR-3B due date of the next financial year.

1. Overview: Why Section 16 Matters

Section 16 of the CGST Act, 2017 is the gateway provision for Input Tax Credit. It defines who is eligible, what conditions must be met, and when the right to credit expires. Every GST-registered business that claims ITC must pass through the four conditions of Section 16(2) — there is no partial compliance. A failure on any single condition disqualifies the credit entirely.

Courts and the GST Council have consistently treated Section 16 as a strict-compliance provision. The Supreme Court, in State of Karnataka v. Ecom Gill Coffee Trading Pvt. Ltd. (2023), affirmed that ITC is a statutory benefit available only upon strict fulfilment of prescribed conditions — it is not an inherent right.

Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in Section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business… — Read the full CGST Act on CBIC.gov.in →

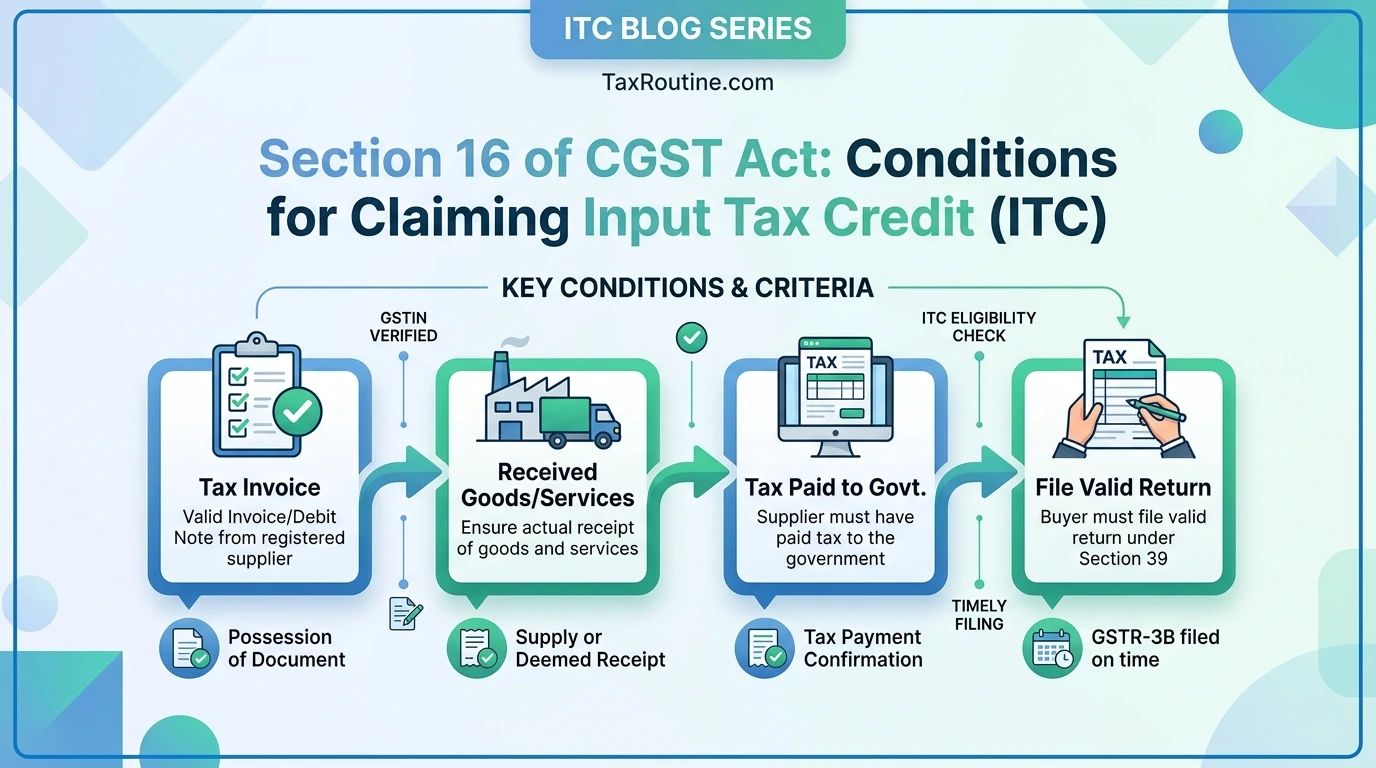

2. The Four Conditions Under Section 16(2)

Section 16(2) is unambiguous: a registered person shall not be entitled to ITC unless all of the following conditions are satisfied simultaneously.

Valid Tax Invoice or Prescribed Document

The registered person must possess a valid tax invoice, debit note, or other prescribed document — issued by a registered supplier — containing all mandatory particulars under Rule 46.

Receipt of Goods or Services

The goods or services (or both) must have been actually received. For goods received in instalments, ITC is available only on receipt of the last lot or instalment.

Tax Actually Paid by Supplier

The tax charged by the supplier must have been actually paid to the government — either in cash or through valid ITC utilisation. This is verified via GSTR-2B on the GST portal.

Return Filed by the Recipient

The registered person (buyer) must have furnished their GST return under Section 39 (i.e., GSTR-3B) for the relevant period.

All four conditions are conjunctive, not disjunctive. Meeting three out of four is not enough. The registered person must satisfy all four conditions simultaneously before ITC can be validly claimed.

3. Condition 1: What is a Valid Tax Invoice?

A tax invoice issued by a registered supplier is the primary document for ITC. Rule 46 of the CGST Rules prescribes the mandatory particulars that every tax invoice must contain:

| Mandatory Particulars (Rule 46) | Consequence if Missing |

|---|---|

| Name, address, and GSTIN of the supplier | Invoice not valid; ITC inadmissible |

| Consecutive serial number (up to 16 characters) | Invoice not valid |

| Date of issue | ITC time-limit computation affected |

| Name, address, and GSTIN of recipient (for B2B) | ITC cannot be linked to recipient |

| HSN code / SAC of goods or services | Invoice not compliant; ITC may be denied |

| Taxable value, rate of tax (CGST/SGST/IGST), and tax amount | Core requirement; absence invalidates invoice |

| Place of supply (for inter-state transactions) | Incorrect tax head applied; ITC disputed |

| Signature or digital signature of supplier | Technically required; enforced in audits |

In addition to tax invoices, ITC can also be claimed on: debit notes issued by supplier, bill of entry (for imports), and an ISD invoice issued by an Input Service Distributor — covered in detail in Part 7 of this series. A proforma invoice or purchase order does not qualify as a valid document for ITC.

4. Condition 2: Receipt of Goods or Services

ITC cannot be claimed merely on the basis of an invoice. The goods or services must have been actually received. This condition addresses phantom invoicing — a major GST compliance concern — where credits are claimed on paper transactions without any actual supply.

Receipt in Instalments — Section 16(2)(b) Proviso

Where goods are delivered in parts or multiple lots — common in construction, manufacturing, and bulk commodity contracts — the proviso to Section 16(2)(b) states that ITC on the invoice is available only upon receipt of the last lot or instalment. Partial credit cannot be claimed on partial delivery.

A contractor orders 1,000 MT of steel to be delivered in 4 lots of 250 MT each

Invoice date: 1 January 2026. Total invoice value: ₹50,00,000 + GST ₹9,00,000.

Delivery 1: 250 MT received on 10 January → No ITC yet.

Delivery 2: 250 MT received on 25 January → No ITC yet.

Delivery 3: 250 MT received on 10 February → No ITC yet.

Delivery 4 (Last lot): 250 MT received on 28 February → Full ITC of ₹9,00,000 available from February return onwards.

Deemed Receipt — Third-Party Delivery

Where goods are delivered to a person other than the registered person — for example, to a job worker or a third-party warehouse on the registered person’s direction — receipt is deemed to have occurred by the registered person as per the explanation to Section 16(2)(b). The registered person’s ITC is not lost merely because goods land at a third-party premises.

5. Condition 3: Tax Must Be Paid by the Supplier

This condition makes ITC inherently dependent on your supplier’s compliance. Even if you hold a valid invoice and have received the goods, you cannot claim ITC if your supplier has not paid the tax to the government. The GST system enforces this through GSTR-2B on the GST portal: invoices appear in GSTR-2B only when the supplier has filed their return and the return contains that invoice.

| Scenario | Appears in GSTR-2B? | ITC Available? |

|---|---|---|

| Supplier filed GSTR-1 and GSTR-3B with the invoice | Yes | Yes |

| Supplier filed GSTR-1 but not GSTR-3B (tax not paid) | No | No |

| Supplier cancelled GST registration after filing | Yes (if return filed before cancellation) | Yes |

| Supplier omitted invoice in GSTR-1 | No | No |

| Invoice uploaded by supplier after cut-off date | Next month | Next period |

Run a monthly reconciliation between your purchase register and GSTR-2B before filing GSTR-3B. Chase suppliers whose invoices are missing from GSTR-2B. Claiming ITC beyond what appears in GSTR-2B exposes you to demand notices and interest under Section 50 — covered in detail in Part 4 of this series.

6. The 180-Day Payment Rule — Rule 37

The proviso to Section 16(2) read with Rule 37 of the CGST Rules introduces a critical obligation on the buyer: if you fail to pay the value of supply plus the tax amount to your supplier within 180 days of the invoice date, the ITC already claimed must be reversed — added back to your output tax liability — along with interest under Section 50. For a practitioner-level deep dive including all the real-world complications this rule creates, see Part 6 of this series: ITC Reversal under Rule 37.

Buyer claims ITC on August invoice but pays supplier only in March

Invoice date: 1 August 2025. ITC claimed: ₹1,80,000 in August 2025 GSTR-3B.

180 days expire: 28 January 2026. Buyer has not paid the supplier.

Reversal required: In January 2026 GSTR-3B → reverse ₹1,80,000. Interest at 18% p.a. from August 2025 to January 2026 (≈ 6 months) = ₹1,80,000 × 18% × 6/12 = ₹16,200 interest payable.

Payment made: March 2026. ITC of ₹1,80,000 can be re-claimed in March 2026 GSTR-3B.

Rule 37A was introduced to handle cases where the supplier has filed GSTR-1 but has not filed GSTR-3B (i.e., tax not deposited). In such cases, the buyer’s ITC is provisionally available but must be reversed if the supplier does not file GSTR-3B by 30th September of the following financial year. This is separate from and in addition to the 180-day buyer-payment rule. See the full Rule 37A analysis in Part 6 of this series.

7. Condition 4: Recipient Must Have Filed Their Return

The fourth condition — Section 16(2)(d) — requires that the registered person (the buyer, i.e., the one claiming ITC) must themselves have filed their return under Section 39, which is GSTR-3B. This condition ensures that the buyer is themselves a compliant taxpayer. Returns are filed through the GST portal at gst.gov.in.

In practice, this means you cannot claim ITC in a period for which you have not filed GSTR-3B. The credit can be claimed in the first return filed after the gap — but subject to the time limit under Section 16(4).

8. Section 16(4): The Hard Time Limit for Claiming ITC

Beyond the four conditions of Section 16(2), the legislature has placed a strict time-based cut-off under Section 16(4). ITC on any invoice or debit note must be claimed by the earlier of the following two dates:

| Cut-off Event | What It Means |

|---|---|

| (a) Due date of GSTR-3B for November of the next FY | For invoices of FY 2025-26, the last date to claim ITC is the due date of filing GSTR-3B for November 2026 (i.e., 20th December 2026 for monthly filers). Amended by Finance Act 2024 — previously it was September. |

| (b) Date of filing the Annual Return (GSTR-9) | If the annual return for FY 2025-26 is filed before 20th December 2026, that filing date becomes the cut-off. ITC cannot be claimed after GSTR-9 is filed. |

Once the Section 16(4) time limit expires, ITC is permanently forfeited. Unlike the 180-day reversal under Rule 37 (where ITC can be re-claimed after payment), there is no mechanism to reclaim lapsed ITC under Section 16(4). The Supreme Court in Union of India v. Bharti Airtel Ltd. (2021) has affirmed the constitutional validity of time-bound ITC restrictions. For interest implications of wrongfully retaining lapsed ITC, see Part 4: Interest under Section 50.

9. Special Situations Under Section 16

9.1 ITC on New Registration — Section 18(1)

A person who obtains GST registration voluntarily or becomes liable to register can claim ITC on stock held on the day immediately preceding the date of registration — for inputs, semi-finished goods, and finished goods held in stock. Capital goods ITC is also available on a depreciation-adjusted basis — the mechanics of this are covered in Part 5: ITC on Capital Goods. The claim must be made within 30 days of becoming eligible.

9.2 ITC After Switching from Composition to Regular Scheme — Section 18(1)(c)

When a composition taxpayer switches to the regular GST scheme, they can claim ITC on all inputs held in stock, inputs contained in semi-finished/finished goods, and capital goods on the day immediately preceding the date of switching. Again, the 30-day window applies.

9.3 ITC Where Depreciation Is Claimed on Tax Component — Section 16(3)

If a registered person claims depreciation on the GST component of the cost of capital goods under the Income Tax Act, 1961, they cannot also claim ITC on that GST amount. It is double-dipping — and explicitly prohibited. The business must choose: either claim ITC (exclude GST from depreciable cost) or claim depreciation on the full cost including GST (and forgo ITC). The full depreciation vs ITC trade-off analysis is in Part 5 of this series.

10. Quick Reference: Section 16 at a Glance

| Provision | Requirement | Consequence of Non-Compliance |

|---|---|---|

| Section 16(1) | Registration + use in course of business | Not eligible to claim ITC at all |

| Section 16(2)(a) | Valid tax invoice / prescribed document | ITC inadmissible; credit disallowed |

| Section 16(2)(b) | Actual receipt of goods or services | ITC inadmissible; demand + penalty risk |

| Section 16(2)(c) | Tax paid by supplier to government | ITC unavailable until supplier pays and it reflects in GSTR-2B |

| Section 16(2)(d) | Recipient has filed their GSTR-3B | ITC cannot be claimed for unfiled periods |

| Rule 37 (180-day rule) | Payment to supplier within 180 days | ITC reversed + interest u/s 50 at 18% p.a.; re-claimable on payment |

| Section 16(3) | No depreciation on GST component | ITC disallowed if depreciation claimed on tax portion |

| Section 16(4) | Claim by November GSTR-3B due date or GSTR-9 date (whichever earlier) | ITC permanently forfeited — no recourse |

Frequently Asked Questions

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- ▶ Part 2 — Section 16: Conditions for Claiming ITC (You are here)

- Part 3 — Blocked Credits under Section 17(5)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- Part 6 — ITC Reversal under Rule 37: Practical Difficulties

- Part 7 — Input Service Distributors (ISD) under GST